Why Waste & Recycling Companies Struggle With Getting Paid (And How We Fix It)

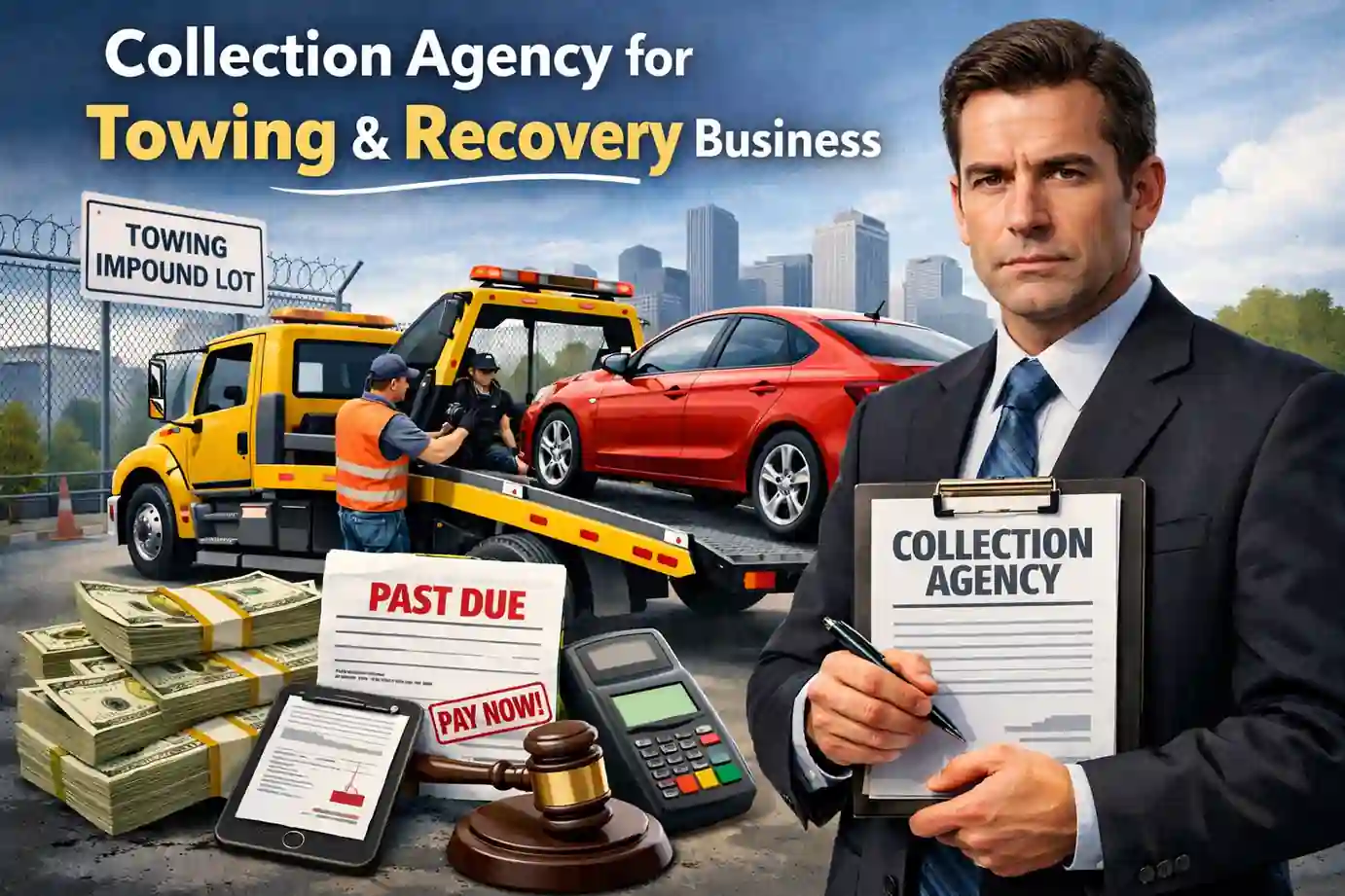

If you run a waste, recycling, or roll-off business, you already know this: picking up trash is the easy part—getting paid is harder.

Fuel, tipping fees, trucks, carts, insurance, safety… everything costs more every year. Yet many customers treat your invoices like low-priority suggestions.

Here’s what we see every day and how we help turn it around.

The AR Problems Every Hauler Recognizes

1. Roll-off jobs that never get paid

You drop a box, haul the debris, send the invoice… and once the container leaves the property, the urgency to pay disappears. After 30–60 days, those balances are on life support.

2. Residential routes with “ghost” balances

Residential customers forget, move, or quietly switch providers. A few unpaid months on a low-rate cart service don’t look like much—until you multiply that across a whole route.

3. Commercial customers playing the float

Restaurants, small shops, and even some property managers treat your invoice as “whenever we can get to it.” You see partial payments, skipped months, and endless promises.

4. Confusing bills that invite disputes

Base fee, fuel surcharge, environmental fee, contamination charges, extra pulls, special pickups… If your billing is complex but your explanation is short, people stall instead of paying.

5. Staff who are too busy to chase money

CSRs and dispatch are buried in route changes, missed-pickup calls, cart swaps, and complaints. Serious AR follow-up slides to the bottom of the list until invoices are 90+ days late and much harder to collect.

How We Help Waste Companies Recover More, With Less Friction

We work only in collections, so we can give your AR the consistent attention it never gets in-house.

-

We can collect in all 50 states and Puerto Rico

-

We use both fixed-fee and contingency programs

-

Our approach is firm but professional, protecting your brand and online reviews while still getting results

Most waste and recycling clients use Step 2 followed by Step 3:

Serving some of the biggest Waste Management Companies NationwideNeed a Collection Agency? Contact Us |

Low-Cost Fixed-Fee Letters (Around $15 per Account- Step 2)

For newer past-due accounts (roughly 30–120 days), Step 2 is usually the best starting point.

For about $15 per account, we send up to five contacts (letters plus optional email/text) under our name:

-

Clear, professional notices referencing service dates, sites, and balances

-

Simple instructions to pay or contact us to resolve any issues

-

Enough pressure to get the honest but “slow” payers moving

Because the cost is fixed and low, you can place a large batch of accounts and quickly see who will resolve with a light push.

Contingency Collections (Typically 40% – Step 3)

For stubborn accounts—older balances, repeat offenders, higher-dollar invoices—we move to contingency collections:

-

No recovery, no fee (we typically keep 40% of what we collect)

-

Collectors who understand waste-industry issues like contamination, overages, and contract minimums

-

Respectful tone to protect your reputation, while still being direct and persistent

-

Payment-plan options and settlement when that yields more cash than “all or nothing” standoffs

This is where we work the accounts your team doesn’t have time (or patience) to chase.

Why Many Haulers Switch to Us

Companies come to us after trying to self-collect or after using another agency that treated them like “just another utility.”

They’re looking for:

-

Better recovery on 60–180-day accounts

-

Cleaner communication with customers and fewer complaints

-

A mix of fixed-fee and contingency that fits their budget

-

A partner that understands routes, carts, roll-offs, and transfer or landfill costs, not just generic invoices

If your aging report is full of old invoices from roll-off jobs, slow-pay commercial accounts, or residential routes, it’s time to change that.

A Simple Way to Start

You don’t need to overhaul your entire process on day one.

Many clients simply:

-

Send us a test batch of older accounts their team has stopped working.

-

Run those through Step 2 and Step 3.

-

Compare what we recover versus what their in-house team or old agency produced.

If you like the results, we help you build a simple placement routine so every month your aging report looks cleaner, your DSO comes down, and your trucks are working for paying customers—not for free.