Most small businesses that fail don’t run out of customers — they run out of cash, usually because of slow-paying accounts. Improving cash flow starts with clear payment terms and prompt invoicing, gets reinforced by consistent follow-up and modern tools like AI-drafted reminders, and ends with knowing when to bring in outside help on accounts that have gone quiet for 60 to 90 days.

Why Cash Flow Problems Sneak Up on Good Businesses

An often-cited stat puts the number at around 80% of small business failures tracing back to cash flow, not a lack of customers or a bad product. The pattern is usually the same: work gets done, invoices go out, and then nothing happens for weeks because no one followed up. None of the fixes below are complicated — most just require deciding in advance what your process is, instead of reacting account by account.

Set the Terms Before You Need Them

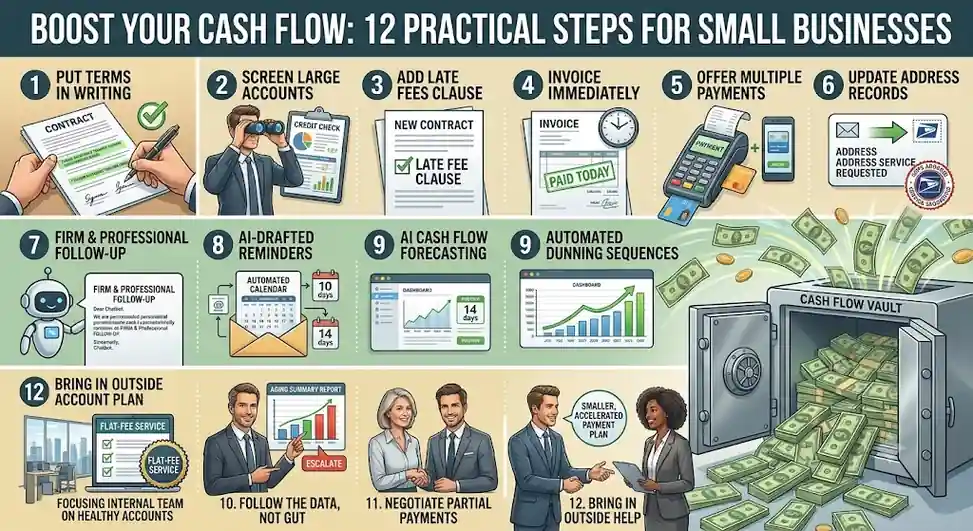

Put payment terms in writing

If customers don’t know exactly when payment is due, plenty will assume “whenever” is close enough. State your terms clearly on every invoice and contract, not just in a conversation that’s easy to forget.

Screen larger accounts before extending credit

A quick bank reference or trade credit check before a large sale on credit is a small cost against a real risk. For mid-sized deals, even a basic credit check pays for itself the first time it flags a problem account.

Add a late fee clause up front

A late fee is easiest to introduce when you’re signing a new agreement — nobody expects to pay late on day one, so there’s no friction. Down the line, it gives slow payers a reason to prioritize your invoice over others, and covers some of the cost of chasing it.

Make It Easy to Pay You Fast

Invoice immediately, then follow up on a schedule

Delayed invoicing is a surprisingly common reason payments are late — the customer simply hasn’t been billed yet. Once an account is overdue, contact every 10 to 14 days rather than waiting a full month between reminders.

Offer more than one way to pay

A customer who has to mail a check or read a card number over the phone is a customer who’ll put it off. Online payment, ACH, and card options remove that friction.

Keep your address records current

Bad addresses are a quiet source of missed payments. USPS’s “Address Service Requested” service (printed just below your return address) automatically returns updated forwarding information when mail goes to an old address — most modern billing platforms now run this check automatically as part of sending statements.

Modern Tools Worth Adding to the Basics

None of this replaces good process, but a few tools have become genuinely useful additions:

- AI-drafted reminders: Tools like ChatGPT can turn “please pay us” into a firm, professional, personalized follow-up in seconds — useful for a business without a dedicated collections writer.

- Automated dunning sequences: Many invoicing platforms now schedule and send reminder sequences automatically, timed around when a given customer segment historically responds.

- AI-assisted cash flow forecasting: Modern accounting software can flag which open invoices are statistically likely to go late based on that customer’s payment history, before the due date passes.

- Basic chatbots for payment status: A simple bot that answers “what do I owe and how do I pay it” frees staff for the calls that actually need a person.

Follow the Data, Not Your Gut

Use your aging report to decide when to escalate

It’s tempting to give a familiar customer more slack because it “feels” like they’ll pay eventually. An aging summary report will tell you faster and more accurately who’s actually paying and who isn’t.

Treat a partial-payment call as a good sign

A customer who calls to say they can’t pay in full is still engaging. Negotiate what they can pay now and when the rest is due — a smaller, aging balance is easier to resolve than a large one that’s gone quiet.

Handle People Well, Fix Your Own Mistakes Fast

Staff dealing with overdue accounts should be trained to stay firm without being adversarial — the goal is getting current while keeping the relationship. If a customer is disputing a charge because of a genuine error on your end, own it and fix it quickly; denying an obvious mistake just adds resentment on top of an unpaid bill. And know the law: businesses collecting their own debts are often bound by many of the same rules that govern third-party collection agencies, including restrictions on when and how you can contact someone.

Know When to Bring in Outside Help

Statistics commonly cited in the collections industry suggest in-house follow-up loses most of its effectiveness after 90 days — by that point, a customer has usually had four to six requests for payment already. That’s the point where a flat-fee reminder service or a collection agency partner tends to accomplish more than another internal phone call, simply because the request is coming from somewhere other than you. Not every account will be collected no matter what you do — the businesses that manage cash flow best are the ones that identify those accounts early and stop spending time on them.

Need help with an account that’s stopped responding? Contact us and we’ll help you find the right fit.

Frequently Asked Questions

What’s the biggest cause of small business cash flow problems?

Slow-paying or non-paying customers, most commonly. Around 80% of small business failures are linked back to cash flow issues rather than a lack of demand for the product or service itself.

How often should I follow up on an overdue invoice?

Every 10 to 14 days once an account is past due. Waiting a full month between reminders lets the balance drift further from the customer’s mind.

Should I charge a late fee?

It’s worth considering, especially if it’s written into the agreement from the start. A late fee gives customers a reason to prioritize your invoice and offsets some of the cost of following up.

Can AI tools actually help with collections?

Yes, at a basic level. AI can draft personalized reminder emails, and modern accounting software can flag which invoices are statistically likely to go late before the due date even passes.

When should I stop chasing an overdue account myself?

Most in-house follow-up loses effectiveness after 90 days. If an account has gone quiet after four to six contact attempts, that’s typically the point to consider outside help rather than continuing to absorb the time cost yourself.

Is it legal to call customers about a past due balance?

Generally yes, but many states hold businesses collecting their own debts to rules similar to those governing collection agencies — restrictions on contact hours and disclosing the debt to third parties, for example. Check your state’s requirements if you’re unsure.