Optometrists examine the eyes for both vision and health problems. They spend years getting the “Doctor of Optometry” degree and then gradually establish their name in the city. It is undoubtedly a promising career since a wave of aging baby boomers will eventually need to see an optometrist at some point in their life. However, optometry practices have their own set of business complications, including overdue accounts receivable.

Need a cost-effective Collection Agency for your unpaid bills? Contact Us |

Optometrists regularly face several business challenges, these include:

1. Managing their employees and retaining quality talent.

2. Keeping up with government regulations.

3. Paperwork associated with running a small business.

4. Low reimbursement rates from government programs like Medicaid or Medicare.

5. Retaining patients when their employer changes vision insurance.

6. Peer competition.

7. How to expand their optometry practice to get new patients.

8. Accounts receivable and unpaid bills.

But when a patient repeatedly fails to make a payment on time, there is little that an optometrist’s office can do. Sending reminder invoices and follow-up calls often do not work. They are met with several excuses from patients, often genuine, sometimes not. In a worst-case scenario, the patient does not pick up the call, or the invoice letter gets returned as “undelivered/wrong address”.

Overdue accounts receivable can hurt the profits of a small business.

Another nightmare scenario can arise if the practice gets sued back by the patient because the in-house staff of the optometrist’s office was not fully aware of the federal and state collection laws involved while trying to recover money on past due accounts and unknowingly commits a violation. These legal complications can be costly and stressful for the practice.

Health insurance or vision insurance plans cover many optometry services. Dealing with insurance companies can complicate the billing process due to reasons like denials, delays, and the need for additional documentation.

Instead of writing off these past-due accounts receivables, transferring them to a professional Debt Collection Agency after 60 or 90 days of non-payment is advisable.

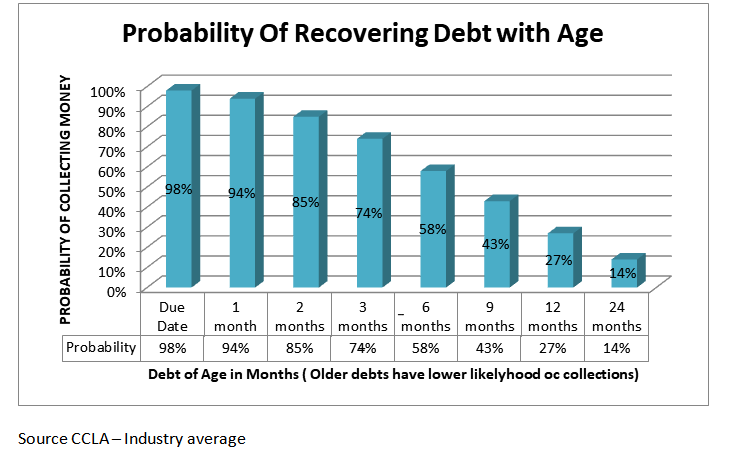

Collection Agencies have sophisticated debt collection techniques and tools to track the debtors and recover money from them. Optometrists can select low-cost diplomatic demand demands service or a slightly more intensive collection calls service. The earlier you transfer an account for collections, the higher the chances you will recover money from it.

Collection agencies are cautious while dealing with medical debt collections. They will try to recover money diplomatically so that the patient-doctor relationships are not strained. Unethical, aggressive, and abusive tactics can ruin your practice’s reputation.

When patients realize that a debt collection agency is involved, they are far more likely to clear their outstanding bills. So, while the optometrist focuses on serving existing clients and expanding his practice, the collection agency acts as an extension of their office, recovering money from past-due accounts.

| Collection Letters Service |

|

| Collection Calls Service |

|

Contact us for your debt collection needs.