In the mortgage sector, a delinquent loan is more than a line item—it represents a high-value asset tied to a sensitive community relationship. With the average cost of a single foreclosure now exceeding $50,000 in legal fees, lost interest, and property maintenance, institutional lenders need a strategy that prioritizes resolution over repossession. Nexa provides the “Velvet Hammer”—a recovery model that balances firm mediation with a “Reputation Shield” to secure your capital without the PR fallout.

Nexa provides a reputation-safe approach, equipped with all 50-state collections license, offering free credit reporting, free litigation, free bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II & GLBA compliant. Over 2,000 online reviews rate us 4.85 out of 5.

Need a Collection Agency? Contact us

Transparent Pricing: The $15 Fixed-Fee vs. Contingency Model

We believe in maximizing your recovery through cost-effective intervention before accounts reach the point of no return.

-

Phase 1: The $15 Fixed-Fee “Early-Out” (Day 45–90):

Ideal for curing delinquency before it hardens. For just $15 per account, we provide diplomatic, third-party outreach. Payments go directly to you, and you keep 100% of the recovered funds.

-

Phase 2: Contingency-Based Recovery (20%–40%):

For aged deficiency balances or “ghosted” borrowers. This is a No Recovery, No Fee model. We utilize high-level skip-tracing and intensive mediation, and you only pay when we successfully return capital to your bank.

Institutional Security: Built for Bank-Level Audits

Mortgage lenders handle the most sensitive Non-Public Personal Information (NPI) in the market. Nexa’s infrastructure is hardened to meet and exceed federal and state examination standards:

-

Compliance Certifications: We are SOC 2 Type II and GLBA compliant, ensuring your data is managed under the highest security protocols.

-

Security Infrastructure: Mandatory Multi-Factor Authentication (MFA) and High-Level VPNs for every employee. All data in transit is protected by PGP encryption.

-

SCRA Compliance: We perform automatic scrubs for the Servicemembers Civil Relief Act, ensuring your institution is never at risk for non-compliant action against active-duty military personnel.

The “Velvet Hammer”: Protecting Your Reputation

Foreclosure is a last resort that can trigger “review-bombing” and community backlash. Nexa rebrands our specialists as “Account Reconciliation Concierges.” We help your borrowers navigate billing confusion or temporary financial hurdles, keeping the dialogue productive rather than adversarial.

-

100% Call Recording: Every interaction is recorded and archived for audit transparency.

-

Random Quality Audits: Our compliance team reviews calls daily to ensure our Concierges remain empathetic and professional.

-

Sentiment Analysis: We use AI-driven monitoring to detect call tension, ensuring your brand is always protected.

Current Regulatory Outlook & State-Specific Realities

Navigating the mortgage landscape in Current years requires a partner who understands the shifting legal ground. Regulatory bodies like the CFPB are increasingly focused on “junk fees” and aggressive servicing tactics.

-

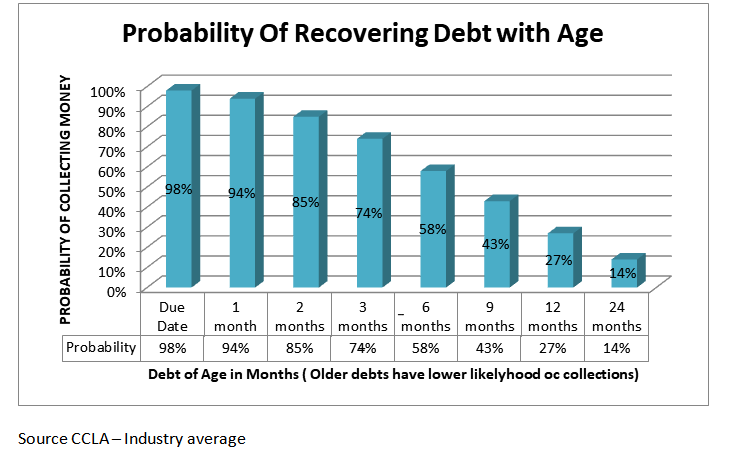

The “90-Day Cliff”: National data shows that once a mortgage is 90 days delinquent, the probability of a “cure” without foreclosure drops by nearly 65%. Our $15 model is designed to intervene at Day 45 to bridge this gap.

-

California (Judicial vs. Non-Judicial): In non-judicial states like California, we focus on high-velocity mediation to avoid the lengthier court process. However, for deficiency balances following a sale, we pivot to asset-searches to determine if a legal pursuit is viable.

-

New York & Florida (The Judicial Hurdle): In states with mandatory judicial foreclosure, our “Velvet Hammer” mediation is critical to reducing the “time-to-recovery,” which can often exceed 600 days in these jurisdictions.

-

SB 1061 & Privacy Trends: While some states are limiting the reporting of medical debt, the ripple effect is a higher consumer focus on credit health. We use this as a mediation lever, helping borrowers understand the long-term benefit of resolving their mortgage deficiency voluntarily.

The Legal Escalation Path: When Mediation Ends

When diplomatic mediation is exhausted, Nexa offers a seamless transition to Legal Escalation. Where state laws permit, we utilize a network of specialized attorneys to pursue Deficiency Judgments.

-

Asset Discovery: Before recommending legal action, we perform a deep-dive skip-trace and asset search to ensure the borrower has the means to pay, saving you unnecessary legal fees.

-

Unified Strategy: Our “Concierges” manage the transition to our legal partners, ensuring a single point of contact for your internal recovery team.

Recent Recovery Results: Institutional Data

-

Regional Bank Portfolio:

A lender in the Northeast had $185,000 in delinquent HELOC balances. Using our Phase 1 ($15 Fixed-Fee) service, we resolved $142,000 within 60 days. The bank retained 99% of the principal with a total collection cost of less than $500. -

Credit Union Mortgage Deficiency:

A local CU was “ghosted” on a $14,500 deficiency balance after a short sale. Our Account Reconciliation Concierges successfully mediated a structured settlement, returning $11,200 in under 45 days without resorting to litigation.

Frequently Asked Questions (FAQ)

Q: How do you handle escrow or insurance-related disputes?

A: Our Concierges are trained to identify when a “non-payment” is actually an escrow calculation error. We act as a mediator between your servicing department and the borrower to clear the confusion before it escalates to a formal dispute.

Q: Can you collect on multi-family or commercial mortgage products?

A: Yes. We have a dedicated B2B division for commercial real estate recovery, utilizing the same “Velvet Hammer” approach for corporate and LLC-held assets.

Q: Do you offer API integration with our servicing platform?

A: Yes. We offer secure RESTful APIs and SFTP batch processing to ensure your core banking system stays synchronized with our recovery status in real-time.

Next Step for Your Institution:

Would you like me to send you a Current 2026 Mortgage ROI Comparison to see how our Fixed-Fee model compares to the cost of standard foreclosure proceedings?

Serving Lenders NationwideNeed an Experienced Agency for Mortgage Collection? Contact Us |