Palm Bay, FL Past-Due Accounts: Keep It Calm. Get It Closed.

Palm Bay runs on precision—Space Coast engineers, skilled trades, and service businesses moving fast between Malabar Road and I-95.

With Melbourne’s medical hub next door and Port Canaveral driving constant commerce, your invoices shouldn’t be the slowest thing in your operation. When accounts drag out, the real damage isn’t just money—it’s momentum, morale, and the awkward tension your staff carries home.

Nexa provides a reputation-safe approach, equipped with all 50-state collections license, offering free credit reporting, free litigation, free bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II & HIPAA compliant. Over 2,000 online reviews rate us 4.85 out of 5.

Need a Collection Agency? Contact us

Straight Pricing (Pick Your Lane, Stay in Control)

You’ve got two clean options with our Account Reconciliation Team:

-

Fixed-fee: $15 (you keep 100% of what’s recovered)

-

Contingency: 40% (no recovery, no fee)

Early assignment changes everything. The sooner you hand off an account, the more likely it resolves with our most amicable strategies—before frustration hardens into refusal.

Money saver tip: Many clients effectively get the fixed-fee service “free” by treating it as a business expense at tax time after consulting their CPA.

Why Palm Bay Businesses Collect More by Staying Human

If you’ve ever watched a rocket countdown on the Space Coast, you know the truth: pressure without control creates a mess.

That’s the problem with arguing. It lights up the room, but it doesn’t always land the payment.

We recover more by working with the account holder—not against them—because people pay the party that makes payment feel doable.

Our style is diplomatic. Firm enough to secure action. Soft enough to protect your reputation.

That’s the Velvet Hammer: strong results, reputation-safe tone, and a clear path to closure.

We also run a Litigation Scrub early. It helps filter riskier situations so your business doesn’t waste time chasing accounts that are more likely to explode into conflict. This is one reason our recovery rates stay higher than industry average.

Fast Resolution Tools: Email, Text, and Bilingual Outreach

A lot of Palm Bay accounts don’t go “bad.” They go quiet.

So we use modern outreach when appropriate and permitted—email and text—because it reduces phone-tag and speeds up decisions.

We also have Spanish-speaking collectors on board, which matters across Brevard County. When language is clear, excuses fade faster.

Most importantly: your employees go back to what they were hired to do—run schedules, manage crews, care for patients, handle vendors.

Not chase payments. Not absorb uncomfortable conversations. Not become the unofficial collections department.

Recent Recovery Results

1) Medical Balance — Palm Bay

The situation: A medical office in Palm Bay had patient-balance accounts piling up after insurance processing. Some patients genuinely misunderstood their responsibility. Others just stopped responding. Front desk staff was stuck re-explaining the same thing repeatedly—while phones kept ringing.

What we did (2–3 steps):

-

Completed account verification with USPS address checks and a bankruptcy screen before contact intensified.

-

Delivered respectful outreach using approved channels, keeping the tone calm and the message consistent.

-

Offered two resolution lanes: a short structured plan or a single payment option, with clear documentation so nobody felt cornered.

Outcome: Accounts started closing without escalation. The office reclaimed time, reduced stress, and avoided reputation fallout.

2) Commercial Invoice — Melbourne

The situation: A B2B service provider in nearby Melbourne had an outstanding invoice that kept bouncing between “AP review,” “waiting approval,” and “next week.” The work was completed. The relationship mattered. But the balance was turning into an internal distraction.

What we did (2–3 steps):

-

Consolidated proof and issued a formal notice through multiple channels to reach the actual decision-maker—not just the gatekeeper.

-

Negotiated human-to-human with a calm, professional stance: confirm the timeline, remove the stall tactics, set a real deadline.

-

Where permitted and if the client chose it, introduced credit reporting as a non-legal lever to encourage closure without court drama.

Outcome: Payment resolved with reputational control intact. No public conflict. No burned relationship. Just a finished account.

Red Flag Box: 3 Palm Bay Collection Mistakes That Quietly Bleed Cash

-

Waiting because “they’re local” — relationships don’t pay bills unless you guide them to action.

-

Letting emotion into the script — one harsh call can trigger review-bombing or a public complaint that costs far more than the balance.

-

Chasing the wrong person — if you never reach the actual decision-maker, you’re collecting “updates,” not money.

A Note from the Account Reconciliation Team

We don’t show up loud. We show up effective.

We verify first, communicate professionally, and keep the temperature low. When someone can pay, we make it easy to do the right thing. When someone is stalling, we tighten the structure until the account closes. That’s the Velvet Hammer: calm pressure, clean documentation, and outcomes you can count.

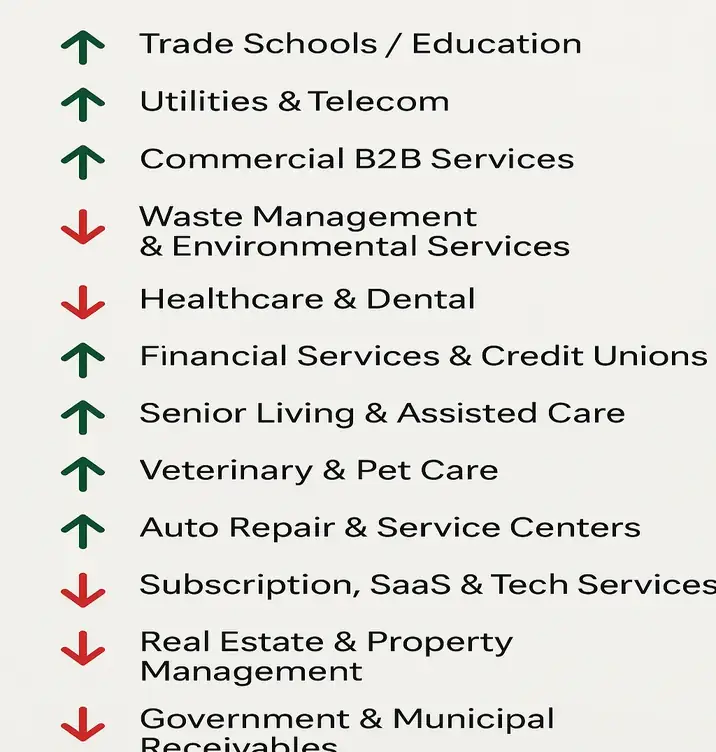

What We Handle Around Palm Bay (Tailored to Local Reality)

-

Healthcare & Medical: Recovery support for hospitals, clinics, and specialty practices with a reputation-safe approach

-

Colleges & Universities: Tuition balances, housing accounts, and administrative fees handled diplomatically

-

Dental: Dental practices and orthodontics—protect patient trust while resolving balances

-

Restoration / Pool / Contractors: Job invoices, change orders, and service agreements without referral-damage

-

K-12 Private & Charter Schools: Enrollment fees, textbooks, and family balances handled with sensitivity

-

Accountants & CPA Firms: Professional fee recovery that respects long-term client relationships

-

Banks & Credit Unions: Delinquent consumer accounts and deficiency balances handled with structured escalation

-

Construction & Trades: HVAC, electrical, and general contractors who can’t afford cash flow disruption

-

B2B Commercial: Vendor invoices, service contracts, and recurring billing across the Space Coast

-

Waste Management: Commercial service billing and route-based balances resolved with consistency

Rules That Matter (Practical, Not Legal Advice)

Florida has state rules for consumer collections and federal standards apply in many situations as well. We stay disciplined: no harassment, no threats, no sloppy third-party talk.

Our process includes USPS address verification, skip tracing, and bankruptcy checks to reduce wrong-party contact and wasted effort.

If you choose and it’s permitted, credit reporting can be used as a non-legal lever.

And for quality protection: calls are recorded and randomly reviewed to prevent rogue behavior and reduce “review-bomb” risk.

FAQs

Palm Bay question: People move often along the Space Coast—what if contact info is outdated?

That’s common here. We run USPS checks and skip tracing so your team isn’t stuck calling dead numbers and leaving voicemails into the void.

What if the account holder says they dispute the balance?

We don’t argue. We isolate the reason, validate the documentation, and offer a structured resolution path that keeps the relationship intact.

Will this damage our reputation online?

Not with Velvet Hammer discipline. Calm language, consistent process, and recorded quality reviews dramatically reduce the blowback that comes from emotional collection attempts.