In the high-stakes world of financial services, your recovery strategy is an extension of your brand’s integrity. For banks, credit unions, and FinTech issuers, a delinquent account is a manageable loss—but a data breach or a regulatory fine is a catastrophic liability. Nexa provides the “Velvet Hammer”: an institutional-grade recovery model that fuses elite cybersecurity with a diplomatic, white-labeled outreach strategy designed to protect your reputation and your bottom line.

Nexa provides a reputation-safe approach, equipped with all 50-state collections license, offering free credit reporting, free litigation, free bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II & GLBA compliant. Over 2,000 online reviews rate us 4.85 out of 5.

Need a Collection Agency? Contact us

Transparent Pricing: Strategic Paths to Capital Recovery

We believe that recovering institutional capital shouldn’t be a financial gamble. We offer a two-tiered pricing model designed to maximize ROI across the entire life cycle of a credit card account:

-

Phase 1: The $15 Fixed-Fee “Early-Out” Program:

Ideal for pre-charge-off accounts (45–90 days past due). For a flat $15 per account, we provide professional outreach. Cardholders pay you directly, and you keep 100% of the recovered funds. This is the ultimate “administrative fix” for early-stage delinquency. -

Phase 2: Contingency-Based Recovery (30%–40%):

For post-charge-off portfolios or aged debt. This is a No Recovery, No Fee model. We utilize intensive skip-tracing and professional mediation, and you only pay a percentage of what is successfully deposited back into your institution.

Secure Your Institution’s Cash Flow – Contact Nexa Today

Bank-Grade Security & Infrastructure: Your Compliance Shield

For financial institutions, security is the primary barrier to entry. Nexa’s infrastructure is engineered to exceed the rigorous audit requirements of the banking industry.

-

SOC 2 Type II Certified: Our internal controls are independently audited to ensure the highest standards of security, availability, and confidentiality.

-

GLBA & Regulation F Compliance: We adhere strictly to the Gramm-Leach-Bliley Act and CFPB Regulation F, ensuring Non-Public Personal Information (NPI) is shielded and dunning frequency is strictly governed.

-

Hardened Connectivity: Mandatory high-level VPNs and Multi-Factor Authentication (MFA) are required for every employee. Data in transit is protected by PGP encryption.

-

PCI DSS Level 1 Standards: As a partner to credit card issuers, we maintain strict payment card industry standards to ensure secure transaction processing without storing sensitive card data.

Technical Integration: Zero-Latency Onboarding

We understand that for modern issuers, manual data entry is a relic. Nexa provides a scalable technical layer that integrates seamlessly with your core banking or Loan Origination System (LOS).

-

RESTful API Ecosystem: We offer secure API endpoints for real-time account placement and status updates, allowing your internal systems to “talk” to our recovery engine instantly.

-

Webhook Event Notifications: Receive automated “pings” the moment a payment is made or a dispute is raised, ensuring your internal ledgers are updated with zero latency.

-

Secure SFTP Batching: For traditional institutions, we support encrypted SFTP batch file transfers for high-volume portfolio management.

The “Velvet Hammer” Philosophy: Protecting Your Institutional Brand

Financial institutions are under constant scrutiny from regulators and the public. A single “rogue collector” can trigger a PR crisis or a regulatory audit. Nexa utilizes The Velvet Hammer approach to mitigate this risk.

We rebrand our specialists as “Account Reconciliation Concierges.” We don’t call to demand cash; we reach out to help your cardholders navigate billing confusion, insurance gaps, or temporary financial hurdles.

-

100% Call Recording: Every interaction is recorded and archived for audit transparency.

-

Random Quality Audits: Our compliance team performs daily reviews to ensure our Concierges remain empathetic and helpful.

-

Sentiment Analysis: We utilize AI-driven analysis to monitor call tone, ensuring your brand is always represented with the highest degree of professionalism.

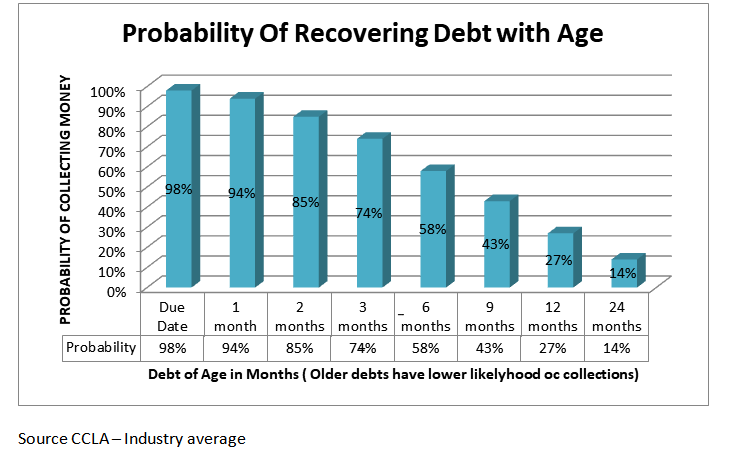

Strategic Intervention: Beating the “90-Day Cliff”

Current industry data shows that the probability of recovering credit card debt drops by nearly 50% once the account passes the 90-day mark. Our strategy is built to intervene before the debt “goes cold.”

-

Pre-Charge-off Early Intervention: By using our $15 Fixed-Fee model at Day 45 or 60, we act as a white-labeled extension of your billing department. This “soft-touch” dunning cycle resolves confusion early and maintains cardholder loyalty.

-

Consumer Self-Service Portal: We provide a 24/7, SOC-compliant payment portal where cardholders can resolve debt, set up installment plans, or dispute charges privately—reducing friction and increasing recovery rates.

Recent Recovery Results: Institutional Case Studies

-

Regional Credit Union Recovery:

A mid-sized CU had $144,500 in delinquent card balances. Using our Phase 1 ($15 Fixed-Fee) service, we recovered $97,800 within 90 days. The total cost to the CU was only $1,500, allowing them to retain 98.5% of the capital. -

FinTech Issuer B2B Recovery:

A digital lender was “ghosted” on a series of commercial card accounts totaling $9,800. Our Account Reconciliation Concierges successfully mediated payment plans, securing full settlements within 21 days while preserving the corporate rapport.

Frequently Asked Questions (FAQ)

Q: Can you collect from cardholders who have moved out of state?

Yes. We are licensed to collect in all 50 states, following the specific debt collection laws of the debtor’s residence.

Q: How do you handle account disputes?

Our specialists are trained in professional mediation. When a dispute is raised, it is immediately logged in our system, and a Webhook notification is sent to your team for review, ensuring full transparency.

Q: Is there a minimum portfolio size?

No. Our $15 fixed-fee model makes it cost-effective to recover even small balances or single-account delinquencies that traditional agencies would ignore.

Recovering Credit Card Debt NationwideContact UsHigher Recovery Rates: Top-Notch Customer Service |