Debt collection lawyers are legal professionals who specialize in recovering debts on behalf of their clients. Their work often involves more complex cases, such as those where the debtor is disputing the debt or has significant assets to pursue. Debt collection lawyers must adhere to all relevant laws and regulations, including those protecting debtors’ rights. Here’s a step-by-step breakdown of how debt collection lawyers typically operate:

- Client Consultation and Case Evaluation: Initially, a debt collection lawyer will meet with the creditor (client) to understand the nature of the debt, review the documentation (contracts, invoices, correspondence), and evaluate the legal merits of the case.

- Investigation and Due Diligence: The lawyer conducts a thorough investigation to verify the debt’s validity, assess the debtor’s financial situation, and identify assets that could be used to satisfy the debt. This might involve background checks, asset searches, and reviewing public records.

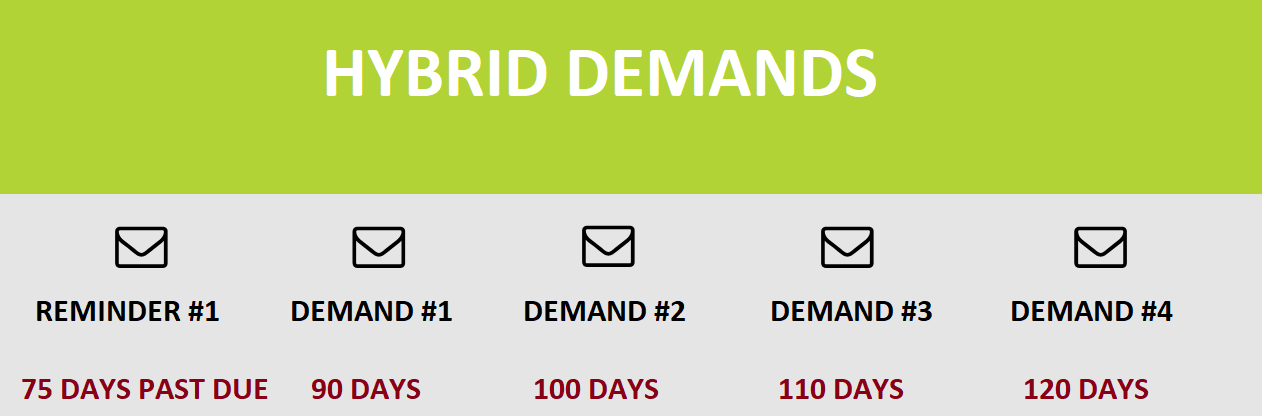

- Demand Letter and Pre-Litigation Negotiations: Before taking legal action, the lawyer often sends a formal demand letter to the debtor, outlining the debt and demanding payment. This letter may also include potential legal consequences if the debt is not settled. The lawyer may engage in negotiations with the debtor or their legal representative to reach a settlement.

- Filing a Lawsuit: If negotiations do not yield results, the lawyer will prepare and file a lawsuit in the appropriate court. This involves drafting and filing a complaint, which officially starts the litigation process.

- Service of Process: The debtor is served with the legal papers, notifying them of the lawsuit and giving them a specific timeframe to respond.

- Litigation Process: The litigation process can include several stages, such as discovery (exchange of evidence), motions (requests for the court to make decisions), and possibly a trial. Debt collection lawyers handle these legal proceedings, advocating on behalf of their clients.

- Obtaining a Judgment: If the case is successful, the court will issue a judgment in favor of the creditor. This judgment legally confirms the debt owed by the debtor.

- Enforcement of Judgment: Once a judgment is obtained, the debt collection lawyer will take steps to enforce it. This could include garnishing wages, seizing assets, placing liens on property, or other legal methods to collect the debt.

- Post-Judgment Actions: In some cases, further legal action may be necessary if the debtor fails to comply with the judgment or if new assets are discovered.

- Settlement or Payment Plans: Throughout the process, and especially once a judgment is obtained, the lawyer may negotiate with the debtor to agree on a settlement or a payment plan that is more manageable for the debtor while satisfying the creditor’s needs.

- Ongoing Communication and Reporting: Throughout the process, the debt collection lawyer keeps the client informed about the progress of the case and advises on the best course of action.

Collection Lawyer Fee

They typically operate on a contingency fee basis, meaning their payment is contingent upon successfully recovering the debt, or they may charge an hourly rate or a flat fee. Contingency Fee ranges from 25% to 50% depending on the amount due, age of the account, jurisdiction and complexity of the case.

Possible out of pocket expenses

There are often out-of-pocket expenses for the creditor in the debt collection process, particularly when using a debt collection lawyer. These expenses can vary based on the complexity of the case, the amount of debt, and the specific actions required. Most of the time, out of pocket expenses include only the court filing fee only ( typically between $250 to $700), however other charges may apply.

Common out-of-pocket expenses include:

- Lawyer’s Fees: Depending on the agreement, creditors might have to pay an upfront retainer fee to the lawyer. While many debt collection lawyers work on a contingency basis (meaning they get paid a percentage of the collected debt), others may charge hourly rates or flat fees.

- Court Costs and Filing Fees: Initiating legal action involves court costs and filing fees, which can vary depending on the jurisdiction and the type of court case being filed.

- Service of Process Fees: There are fees associated with formally serving legal documents to the debtor. These services are typically carried out by professional process servers or law enforcement officers.

- Administrative Costs: These include costs for mailing, copying, and other administrative activities necessary for preparing and managing the legal case.

- Investigative Expenses: If the lawyer needs to conduct investigations to locate the debtor or identify assets, there might be additional costs for services like asset searches, background checks, or hiring a private investigator.

- Expert Witness Fees: In some complex cases, especially those involving large debts or complicated financial matters, it may be necessary to hire expert witnesses. Their fees can be substantial.

- Post-Judgment Enforcement Costs: Even after obtaining a judgment, there might be additional costs associated with enforcing it, such as fees for garnishment, seizing assets, or conducting a sheriff’s sale.

- Interest and Late Fees: If the debt collection process takes a long time, the amount of interest and late fees accumulating on the principal debt can also be considered an indirect out-of-pocket expense.

- Settlement Costs: If a settlement is reached, the creditor might have to bear certain costs associated with drafting and finalizing the settlement agreement.

It’s important for creditors to discuss potential costs with their debt collection lawyer upfront to understand the financial implications of pursuing the debt to avoid possible surprises during the due course of collection. They should also discuss their policy in case the debtor counter-sues the creditor.

Also, creditors should consider the cost-benefit analysis of pursuing the debt, as the costs of collection can sometimes approach or even exceed the amount of the debt itself.