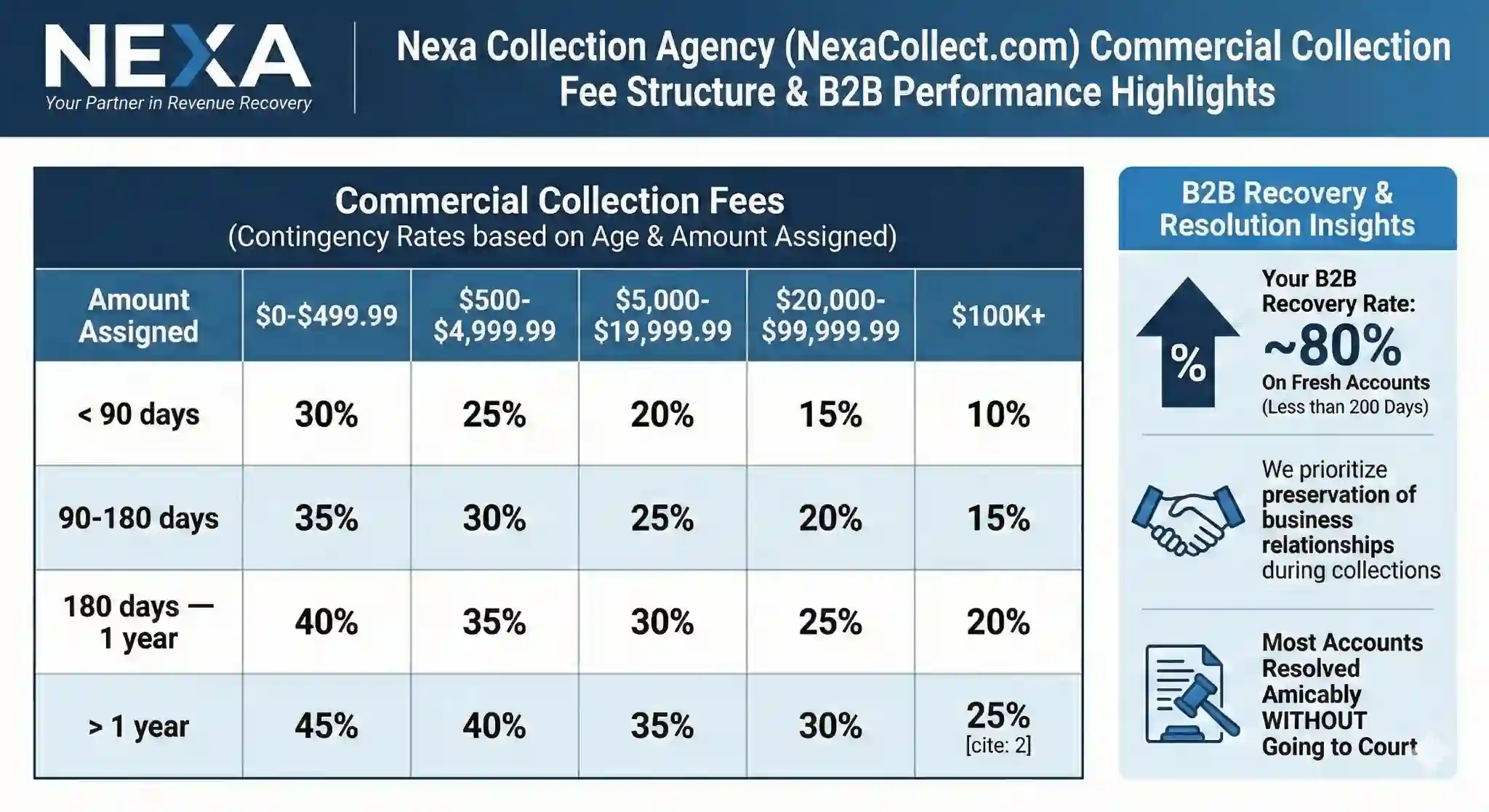

An average collection agency will recover about 20% of the total debt assigned. Some clients may get a 100% recovery rate, for others it could very well be 0%. Here are the most important factors which decide how much a collection agency will collect for you:

1. Collection Agency itself:

A collection agency that follows a friendly approach makes persistent contacts, follows legally complaint tactics, yet a firm approach will recover maximum money. They must know how to recover the debt diplomatically instead of forcefully. Debtors are less likely to pay when they feel threatened.

Since all collection calls are recorded, it is important for the management/supervisor to randomly examine at least a few collection calls daily and discuss shortcomings with their debt collectors. They must have at least a few bilingual debt collectors in order to recover from people who prefer talking only in Spanish. Their debt collectors must be located in multiple time zones in order to work with debtors nationwide.

2. Is your debt primarily Commercial (B2B) or Consumer (B2C)

Commercial debts have a recovery rate of around 75% on viable accounts. For consumer debts, this figure drops to approximately 12%. Factoring in both types of debts, the average recovery rate is about 20%.

3. Age of your debts

Accounts that are assigned around 90 days have an excellent recovery rate, while accounts that are older than one year have a poor recovery rate.

4. Your Industry

Commercial Debts: Nearly 75% recovery rate on viable debts.

These industries have a higher recovery rate: (Over 40%)

College/Universities/ Prof. School, Fuel/Oil/Propane, Printing, Lawn & Garden, Snow Removal, Business Services, Plumbing, Heating, Air, Engineering, Interior Design, Restoration, Publishing and Credit Unions.

These industries have a moderate recovery rate: ( 25%-40%)

Pest Control, Aviation, Media, Industrial, Optometrists, Dental, Personal Services, Funeral services, Repairs, Waste Management, Day Care, CPA / Accountants, Utilities, Government, Member Organizations, Farm Supply, Auto Dealers, Cleaning Service, Fire, Education Schools Misc., Telephone Communications, Elementary/ High School and Medical.

These industries have an average recovery rate ( 15% -25%)

Social Services Misc., Trucking, Veterinarian, Clothing, Manufacturing, Computer Services, Pharmaceutical, Medical supply, Drug Store, Newspaper, Rentals Equipment, Wholesale, Durable, Hotel, Non-Profit and Insurance.

These industries have a lower recovery rate: ( Below 15%)

Chiropractor, Nursing Homes, Banks, Bail Bonds, Property Management, Financial, Legal Services / Lawyers, Gym/Sports Organizations, Electronics, Moving/storage and Real Estate Agents.

5. Quality of your own debt:

If you primarily serve a lower income group, or if your state debt laws are favorable for debtors, then the recovery rate will be lower. Additionally, if your debt is too old then your recovery will decrease.