Whether you manage a small business or a medical practice, overdue accounts come with the territory. These inevitable payment delays eventually force you into a high-stakes ‘Awkward Conversation’ where you shouldn’t have to choose between getting paid and staying professional.

At Nexa, we specialize in the Velvet Hammer approach. We know you want to protect your cash flow without burning bridges or damaging the goodwill you’ve worked years to build. You can have these conversations without confrontation by implementing a structured, professional communication style.

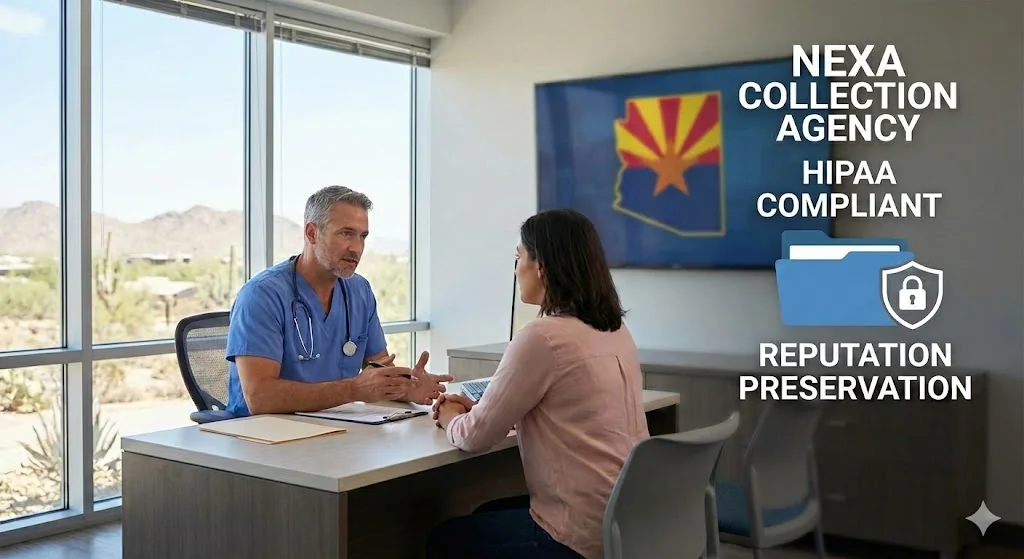

Nexa provides a reputation-safe approach, equipped with all 50-state collections license, offering free credit reporting, free litigation, free bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II & HIPAA compliant. Over 2,000 online reviews rate us 4.85 out of 5.

Need a Collection Agency? Contact us

The “Curious Consultant” vs. The “Aggressive Collector”

The most effective payment conversations don’t start with a demand; they start with a question. By assuming the delay is a simple administrative error or a temporary cash-flow “hiccup,” you lower the debtor’s defenses.

Scenario 1: The “Forgetful” Customer

The Situation: The invoice is 15 days past due. They’ve been a loyal customer for years.

-

The Wrong Approach: “You’re late. When can we expect the check?”

-

The Velvet Hammer: “Hi [Name], I’m just calling to make sure you received the invoice from the 1st. We haven’t seen the payment come through yet—is there anything on our end we need to update or resend to make this easier for you?”

-

Why it Works: It gives them an “out” (an administrative error) while firmly establishing that you are tracking the balance.

Scenario 2: The “Dissatisfied” Delayer

The Situation: The customer is using a minor service complaint to justify holding up a large payment.

-

The Wrong Approach: “That’s not what we agreed on. You still have to pay the full amount.”

-

The Velvet Hammer: “I hear your concerns about [Issue]. Let’s do this: I’ll look into that specific item immediately. In the meantime, can we settle the undisputed portion of the bill today so we can keep the account current?”

-

Why it Works: It separates the “dispute” from the “debt,” preventing them from using a small problem to freeze your entire cash flow.

Scenario 3: The “Ghost”

The Situation: Multiple emails and invoices have gone unanswered.

-

The Wrong Approach: Sending the same invoice for the 5th time.

-

The Velvet Hammer: A brief, professional phone call: “Hi [Name], we’ve reached out a few times regarding your balance. We value our relationship and want to resolve this before it moves into our formal escalation phase. What’s the best way to get this closed out today?”

-

Why it Works: It introduces the concept of “consequences” (escalation) without using threats, forcing a decision.

Three Rules for Every Payment Call

-

Be Calm and Consistent: If you sound stressed, they will mirror that stress. Stay businesslike.

-

Use “We,” Not “You”: “How can we resolve this?” sounds collaborative. “You need to pay” sounds accusatory.

-

Offer a Lane out: Sometimes a customer is genuinely struggling. Offering a 2-part split payment can secure the funds faster than demanding a lump sum they don’t have.

When to Stop Talking and Start Escalating

If a conversation has happened twice and the commitment was broken, the “relationship” is already being damaged by the debtor, not by you. This is the point where third-party intervention saves your time and your sanity.

Two Lanes to Restore Your Cash Flow

-

Fixed-fee $15: Ideal for small balances like membership dues or service no-shows. You keep 100% of the money we recover.

-

Contingency (40%): No recovery, no fee. Best for larger medical spa balances or older accounts that require intensive skip tracing.

Need a Collection Agency? Contact us