A small business collection agency recovers unpaid invoices and overdue accounts on behalf of independent businesses, freelancers, contractors, and service providers — both from other businesses (B2B) and from individual customers (B2C). Unlike large corporate debt collection, small business recovery requires balancing legal leverage with relationship preservation: the client who owes you $800 today may be your best referral source next year. The most effective small business collection agencies combine diplomatic outreach with structured escalation, and work on contingency — meaning no fee unless money is recovered.

You did the work. You delivered the product. You sent the invoice. And then… silence, or excuses.

In small business, an unpaid invoice isn’t just a “late payment”—it’s a Cash Flow Crunch. Whether you’re a B2B consultant or a B2C home service provider, every day that balance sits on your aging report, your profit evaporates.

The secret to recovery isn’t being “the heavy”—it’s Diplomacy. You want your money, but you also want to protect your local reputation and your professional bridges.

Need a Collection Agency for your Business?Contact us• Nationwide Coverage • US Citizens-Only Team • High Recovery Rates • Free Bankruptcy screening • Free Credit Bureau reporting • Free skip tracing • 5-star rated • 24×7 Secure Portal • Industry Specific Collectors • Cost-Effective • No Onboarding fee or Minimums |

The Real Cost of an Unpaid Invoice (It’s More Than the Balance)

Small business owners often delay acting on overdue accounts because the collection agency fee feels like an extra cost. In reality, doing nothing is the most expensive choice. Here is what an unpaid invoice actually costs you:

- Staff time: The average small business owner or office manager spends 3–5 hours per overdue account on follow-up calls, emails, and documentation. At a $75/hr equivalent, a single unresolved $500 invoice can cost more in staff time than it’s worth — before you’ve even considered writing it off.

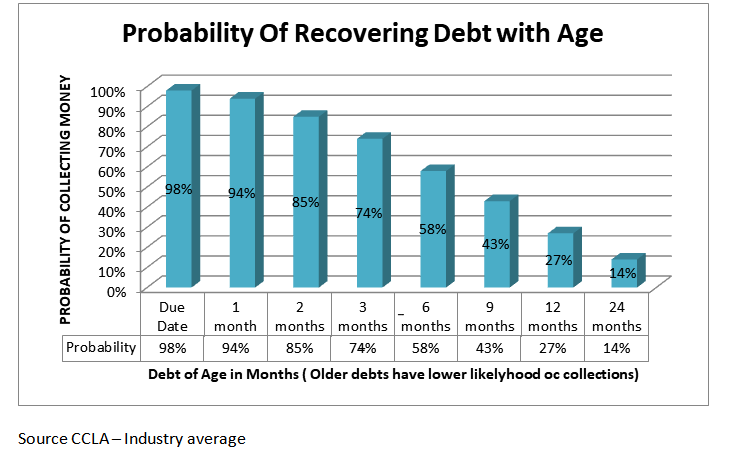

- Recovery probability drops fast: A debt that is 30 days old has roughly a 93% chance of collection. At 90 days, that drops to around 73%. At 6 months, it’s below 50%. Every month of delay costs you approximately 10% of the recoverable value (Commercial Law League of America).

- Cash flow compounding: An unpaid $2,000 invoice doesn’t just cost $2,000. If that cash would have covered materials for your next job, you may need a short-term loan — adding interest cost on top of the lost revenue.

- Opportunity cost: Every hour your team spends chasing a non-paying client is an hour not spent serving paying ones, generating new leads, or improving operations.

The math on hiring an agency: Nexa’s Step 1 fixed-fee collection service costs $15 per account. If it recovers a $300 balance, your net recovery is $285 — and you invested zero staff hours. Even at our 40% contingency rate for larger accounts, recovering $5,000 nets you $3,000 you would not have otherwise seen.

Before You Call a Collection Agency: 6 Steps to Try First

A reputable collection agency is the right move when internal efforts have been exhausted — but doing these six steps first maximizes your recovery odds and gives you stronger documentation when you do place the account:

- Send a formal written invoice with a clear due date. Verbal agreements and informal emails don’t create the paper trail that supports collection. A dated invoice with itemized services, the total due, and a specific payment deadline is your first legal document.

- Frame your first follow-up as a “billing error check.” Your first call or email should give the client a graceful exit: “I wanted to check whether our invoice reached the right department — sometimes things get misdirected.” This lowers defenses and gets a response without triggering conflict.

- Escalate to a decision-maker. If your contact isn’t responding, go up one level. In B2B, find the CFO or business owner directly. In B2C, confirm you’re speaking with the person legally responsible for the bill. Changing stories between contacts are a warning sign — document everything.

- Offer a structured payment plan in writing. Many clients who go silent are embarrassed, not malicious. A written offer of “pay $X now and $Y in 30 days” lowers the psychological barrier and creates a documented commitment. Include a clause that the full balance becomes due immediately if any installment is missed.

- Send a formal final demand letter. This is a written notice — ideally via certified mail — stating the exact amount owed, the deadline for payment, and the consequence of non-payment (referral to a collection agency). Keep it professional, not threatening. A well-crafted final demand letter resolves 20–30% of delinquent accounts without further escalation.

- Stop all new work or services immediately. If the invoice is unpaid and no payment plan is in place, do not continue providing services. Your time and materials are your inventory — delivering more while a balance is outstanding increases your risk with no corresponding leverage.

If all six steps have been attempted and the account remains unresolved past 60–90 days, the time and cost of further internal effort almost always exceeds the cost of placing it with a collection agency. That’s the moment to call us.

The Psychology of Non-Payment: Why They “Ghost”

Whether it’s a CEO or a homeowner, the reason for silence is usually the same: Embarrassment.

* The Business Client: Often stuck in “Decision Paralysis” due to internal budget shifts.

The Individual Customer: Often overwhelmed by personal financial stress.

Nexa acts as your Neutral Mediator. We lower the heat, shifting the conversation from a “confrontation” to a “resolution.” We preserve your brand while we secure your profit.

The Nexa “Dignity-First” Recovery Ladder

We separate “administrative confusion” from “bad debt” to maximize your recovery while protecting your reputation.

Step 1: The Account Reconciliation (Fixed Fee – $15)

Ideal for accounts 60–90 days past due. This is a soft, third-party “nudge” that identifies simple misunderstandings, insurance gaps (for B2C), or internal billing errors (for B2B). You look professional, not desperate—and you keep 100% of the money recovered.

Step 2: Full-Service Mediation (Contingency)

For aged debt or unresponsive people/entities. We perform deep-data scrubs to find the decision-makers and the funds. We use Diplomatic Negotiation to resolve the balance without litigation whenever possible. No Recovery = No Fee.

B2B vs B2C: How Small Business Collection Works Differently

Whether your debtor is another business or an individual customer changes the legal tools, relationship stakes, and recovery strategy. Here’s what you need to know:

| Factor | B2B (Business Client) | B2C (Individual Customer) |

|---|---|---|

| Governing law | UCC (Uniform Commercial Code), contract law — fewer debtor protections | FDCPA — strict rules on contact times, frequency, and language |

| Typical debt size | $500–$50,000+ (invoices, service contracts, project fees) | $50–$5,000 (service calls, co-pays, one-time work orders) |

| Who owes you | A company (may have a slow AP department, not a bad actor) | An individual (may be cash-strapped, embarrassed, or disputing) |

| Relationship stakes | High — a recovered B2B client can become a repeat account worth 10x the invoice | Moderate — a satisfied B2C customer refers neighbors; a bad experience gets reviewed online |

| Leverage tools | Business credit reporting (D&B, Experian Business), UCC liens, vendor reference threats | Consumer credit reporting (note: under $500 no longer reported as of 2024+) |

| Best approach | Diplomatic mediation first; frame as “accounts payable resolution” not collections | Empathy-led outreach; offer payment plans; avoid escalation language until Step 3 |

| When to place | 60–90 days past invoice due date with no payment plan in place | After 2 statements + 1 phone attempt with no response, typically 45–60 days |

Small Business Collection by Industry: How We Tailor the Approach

Not every unpaid invoice is the same. Here’s how collection strategy shifts by industry type — and why it matters for your recovery rate:

Freelancers & creative professionals (designers, writers, photographers)

Freelance debt is often complicated by scope disputes: the client claims the work wasn’t what they asked for. Our collectors are trained to anchor the conversation to the original brief, approved deliverables, and any sign-off communication — shifting the burden of proof back to the debtor. We never accept a vague “I wasn’t happy” as a valid dispute without documentation.

Contractors & trades (HVAC, plumbing, electrical, landscaping, cleaning)

Service contractors often lack formal contracts — relying on verbal agreements, text estimates, or work orders. We work with whatever documentation exists: photo evidence of completed work, text confirmations, or even a counter-signed estimate. For B2C trades where the balance is under $1,500, our $15 fixed-fee demand letter service has a very high resolution rate because many customers simply needed formal notice.

Staffing & recruiting agencies

Staffing debt is almost always B2B — a business that used your placed workers but isn’t paying the invoice. These are typically strong collection candidates because the debtor company is still operational, the work is documented, and the relationship was commercial from the start. We use business credit bureau leverage (D&B reporting) as a primary tool here — it’s highly effective for companies concerned about vendor relationships.

Consultants & professional services (IT, marketing, accounting, legal support)

Professional service disputes often center on “I didn’t see the value” — a subjective objection that can stall collection indefinitely. Our process requires documented scope-of-work and deliverable confirmation before outreach begins, so we can counter any value dispute with objective evidence. We also have strong success rates on partially-paid consulting accounts, recovering the remaining balance after a client stops mid-engagement.

Retail & e-commerce (B2B wholesale, trade accounts)

Wholesale and trade account debt is pure B2B — governed by UCC provisions and typically tied to purchase orders, delivery receipts, and terms agreements. Our collectors understand commercial trade credit environments and can navigate AP departments, dispute procedures, and purchase order discrepancies to recover net-30 and net-60 balances efficiently.

Home services & property management (real estate, maintenance, renovation)

Property-related debt has unique legal leverage: in most states, unpaid contractors can file a mechanic’s lien against the property — a powerful tool that makes the debt follow the asset even if the owner sells. We identify lien eligibility on every property-related account and flag it to our affiliated attorney network when appropriate.

Childcare, tutoring & personal services

These are relationship-sensitive B2C accounts where the provider and client may still see each other in the community. Our dignity-first approach is calibrated for exactly this scenario — professional but non-confrontational, focused on resolution rather than pressure, and designed to leave the door open for the client to return if circumstances change.

Why Small Businesses Choose Nexa

-

The Reputation Shield: One bad review on Google or Yelp can kill a small business. We record and audit all calls to ensure your clients and customers are treated with extreme respect.

-

FDCPA & HIPAA Ready: We handle the legal “alphabet soup” so you don’t have to. We ensure every B2C interaction is 100% compliant with consumer protection laws.

-

The “Audit” Reframe: We don’t call as “debt collectors.” We call as your “Account Reconciliation Partners.” This lowers defenses and leads to faster payments.

Frequently Asked Questions: Small Business Debt Collection

What can I do if a client won’t pay my invoice?

Start by sending a formal written invoice with a clear due date, then follow up with a diplomatically framed call framing it as a “billing error check.” If two statements and a phone attempt haven’t resolved it within 45–60 days, send a formal final demand letter. If that fails, place the account with a collection agency — ideally before 90 days, since recovery rates drop significantly after that point.

Can a collection agency collect without a signed contract?

Yes. While a signed contract is the strongest documentation, collection agencies can work with alternative evidence of the debt: email confirmations, signed work orders or estimates, text messages agreeing to terms, invoices that were not disputed within a reasonable time, and proof of delivery or completed work. The stronger your documentation, the higher the recovery rate — but lack of a formal contract is not a barrier to collection.

How long should I wait before sending an invoice to collections?

The industry benchmark is 60–90 days from the invoice due date, assuming you’ve made at least two statement attempts and one phone contact without success. Waiting beyond 90 days reduces your recovery probability by roughly 10% per additional month. If the client has gone completely silent (“ghosting”), the 60-day mark is early enough to act — silence is a stronger indicator of non-payment than a disputed invoice.

What percentage does a small business collection agency charge?

Nexa Collections offers a fixed-fee service starting at $15 per account for demand letters on newer balances — you keep 100% of what’s recovered. For older or more complex accounts requiring phone outreach, we charge a contingency of 20–40% of the amount collected, depending on account age and balance size. Legal escalation carries a 50% contingency and requires your explicit approval. You pay nothing if we recover nothing.

Will using a collection agency damage my relationship with the client?

Not necessarily — and for newer accounts, often the opposite is true. Our Step 1 first-party reminder service contacts the client as if the message is coming from your business, not from a collection agency. Many “non-paying” clients are simply embarrassed or disorganized, and a professional, structured follow-up resolves the account without any conflict. Even our third-party steps are designed to be diplomatic, not adversarial — our goal is resolution, not confrontation.

Can you collect from a business that has closed down?

Possibly. If the owner operated as a sole proprietor or signed a personal guarantee, personal liability applies. If the business transferred assets to a new entity before closing (successor liability), we investigate whether those assets are reachable. If the closure was a formal bankruptcy filing, collection must stop immediately — we run bankruptcy scrubs on every account to avoid violations. We’ll assess your specific situation and give you an honest recovery probability before you place the account.

Is it worth hiring a collection agency for small amounts under $500?

Yes — especially with our fixed-fee service. At $15 per account for a demand letter campaign, recovering a $200 balance nets you $185 with zero staff hours invested. More importantly, if you have multiple small accounts (10 customers owing $150 each = $1,500), the aggregate makes collection highly cost-effective. Letting small balances age until they’re uncollectable is always the more expensive choice.

What happens if the debtor ignores the collection agency?

If a debtor remains unresponsive after demand letters and phone outreach, we have several escalation options: business credit bureau reporting (for B2B accounts, we report to Dun & Bradstreet and Experian Business), skip tracing to locate a debtor who has moved, and — with your explicit approval — referral to an affiliated commercial attorney for legal action. The specific path depends on the debtor’s asset profile and your appetite for escalation.

Can you collect from a client in another state?

Yes. Nexa is licensed to collect in all 50 states and Puerto Rico, and works with affiliated attorneys in every jurisdiction for legal escalation. Interstate B2B collection is entirely routine for us. State-specific statutes of limitations and contact rules are factored into our outreach strategy for every account we place.

What is skip tracing and when is it used?

Skip tracing is the process of locating a debtor who has moved, changed contact information, or is deliberately evading contact. We use a combination of public records, credit bureau data, social media, and proprietary databases to build a current contact profile. We offer free skip tracing on all accounts — it’s included in our standard service, not charged as an add-on. If a debtor has genuinely disappeared, skip tracing is often what separates a recovered account from a write-off.

How do I get started — what information do you need?

To place an account, we need: the debtor’s name and last known contact information, the amount owed, the date the debt was incurred or the invoice due date, and any documentation you have (invoice, contract, work order, email chain). We accept individual accounts or batch placements via our 24×7 secure online portal. There are no minimum balances, no minimum volumes, no onboarding fees, and no contracts. You can start with a single account and scale from there.

Act Fast!