Early Commercial Recovery: The “Golden Window” for B2B Debt

In commercial lending and B2B sales, the clock ticks faster than in consumer debt. A business that owes you money today might be insolvent, acquired, or bankrupt tomorrow.

The 2026 Reality: The average B2B recovery rate for accounts under 90 days old is nearly 80%. Once that debt hits 6 months, the success rate plummets to roughly 50%. By one year, you are fighting for pennies.

Waiting for a “miracle payment” isn’t patience—it’s a liability. Here is why smart CFOs and Credit Managers assign accounts to third-party collections the moment internal efforts stall.

3 Numbers That Define B2B Collections

-

11% Drop Per Month: Industry data shows that the collectability of a commercial invoice drops by approximately 11% for every 30 days it remains past due.

-

$25,000+: The average commercial collection claim is significantly higher than consumer debt. You cannot afford to treat a $25,000 invoice with the same passive strategy as a $100 utility bill.

-

45% Higher Response: Modern agencies use SMS and digital demand signals, which see a 45% higher response rate from business owners than traditional mail.

The “Relationship Paradox”: Why Outsourcing Saves Clients

Business owners often fear that hiring a collection agency will “nuke” the relationship. The opposite is usually true.

-

The “Buffer” Effect: When you call for money, it gets personal. When we call, it’s business. We act as the “bad cop,” allowing your sales team to remain the “good cop.”

Use a collection agency that starts contacting with a gentle reminder, and then gradually shifts to a more diplomatic/pressurizing approach.

-

The Excuse Remover: Delinquent clients often dodge your sales reps because they are embarrassed. Once an agency steps in, the awkwardness is removed from your direct relationship. We settle the debt so they can buy from you again.

Step-by-Step: How We Recover Commercial Debt

We don’t just “dial for dollars.” Commercial recovery is a forensic process.

1. The “Deep Scrub” (Investigation)

Before we make a call, we investigate. Is the debtor still in business? Have they filed for bankruptcy? Are they paying other vendors but stiffing you? We use skip tracing and commercial credit data to see their financial health.

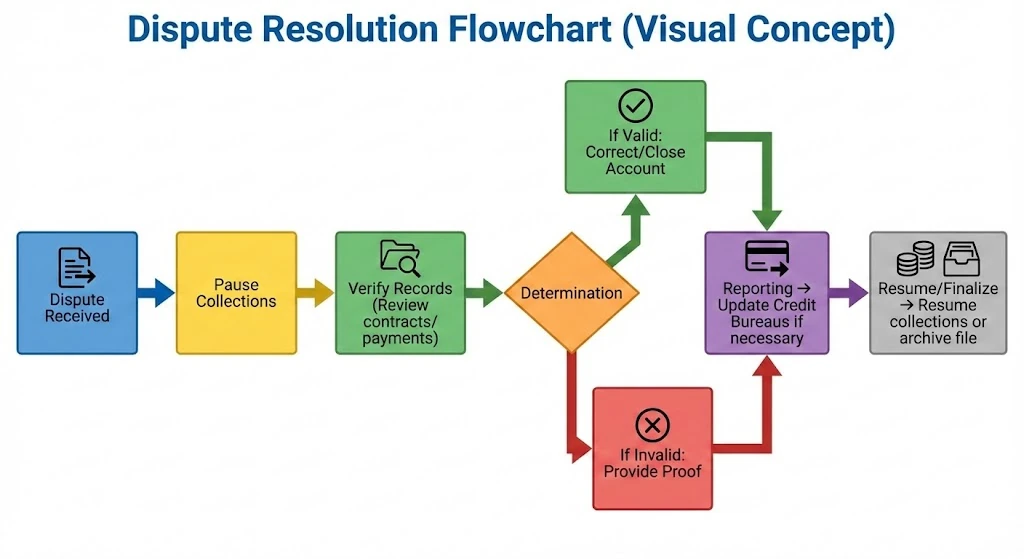

2. The Demand & Dispute Resolution

B2B debts are rarely about “I don’t have money.” They are usually about disputes (e.g., “The shipment was late,” “We didn’t authorize that charge”). Our collectors are trained to cut through these stalls. We demand proof of the dispute or payment in full.

3. The Leverage (Credit Reporting)

For a business, credit is oxygen. We report delinquent commercial accounts to major business credit bureaus. The threat of losing their ability to get a line of credit or a supplier loan is often the only motivation they need to pay.

4. The Settlement Negotiation

If a debtor is truly cash-strapped, we negotiate a Consent Judgment or a structured payment plan that ensures you get paid first, before their other creditors.

Specific Issues We Solve for B2B Creditors

-

“The Check is in the Mail” Stall: We hold them accountable to specific dates and tracking numbers.

-

Unauthorized “Net-Terms” Extensions: Clients who unilaterally decide to pay in 60 days when your terms are Net-30.

-

Supply Chain Excuses: We separate legitimate logistics issues from cash-flow stalls.

-

Ghosting: When the Accounts Payable manager suddenly stops replying to emails.

When to Assign? (The Red Flags)

Do not wait for 120 days. Assign the account immediately if:

-

The debtor has broken two promises to pay.

-

The phone line is disconnected or the website is down.

-

They suddenly switch to a new bank or ask for unusual payment changes.

-

A competitor tells you they haven’t been paid either.

Stop financing your customers’ businesses interest-free.