A commercial collection agency specializes in recovering unpaid invoices and past-due debts between businesses (B2B). Unlike consumer debt collection — which is tightly regulated by the FDCPA — commercial recovery operates under the Uniform Commercial Code (UCC) and contract law, enabling faster timelines, credit bureau leverage, and tools like UCC-1 filings and mechanic’s liens. Businesses typically engage a commercial collection agency when internal accounts receivable efforts have failed and outstanding invoices are 60–120+ days past due.

Commercial debt collection — also called B2B collections — is the process of recovering money owed by one business to another. These disputes often involve complex contracts, purchase orders, freight bills, and multiple decision-makers across departments. At Nexa Collections, we serve CFOs, accounts receivable teams, small businesses, and enterprise companies nationwide, combining diplomatic professionalism with proven legal leverage to recover what you’re owed — without destroying the relationships that matter.

Unpaid invoices are not just an inconvenience; they are a direct threat to cash flow. Research from the Commercial Law League of America shows that a debt only 90 days old has a 73% chance of recovery — but that number falls by roughly 10% for every additional month it goes unpaid. Acting fast is the single biggest factor in successful commercial debt recovery.

Trusted by businesses nationwide to recover millions in lost revenue annually. We combine a 80% success rate on viable claims with a diplomatic “Velvet Hammer” approach—ensuring you get paid without damaging valuable B2B relationships.

When Should You Hire a Commercial Collection Agency?

Most businesses should consider engaging a commercial collection agency when:

- An invoice is 60 or more days past due with no payment or payment plan in place

- A debtor has stopped responding to your calls, emails, or mailed notices

- A client disputes the invoice but has not provided a legitimate counter-claim or documentation

- Internal AR staff are spending more than 2 hours per week chasing a single account

- You suspect a business has changed names, moved, or is preparing to close

- The outstanding balance is large enough to affect your operating cash flow

The 60-day mark is the industry benchmark because recovery rates remain highest before the 90-day threshold. Every month of delay costs you roughly 10% of the recoverable value (Commercial Law League of America).

Quick Facts: Why Choose Us?

-

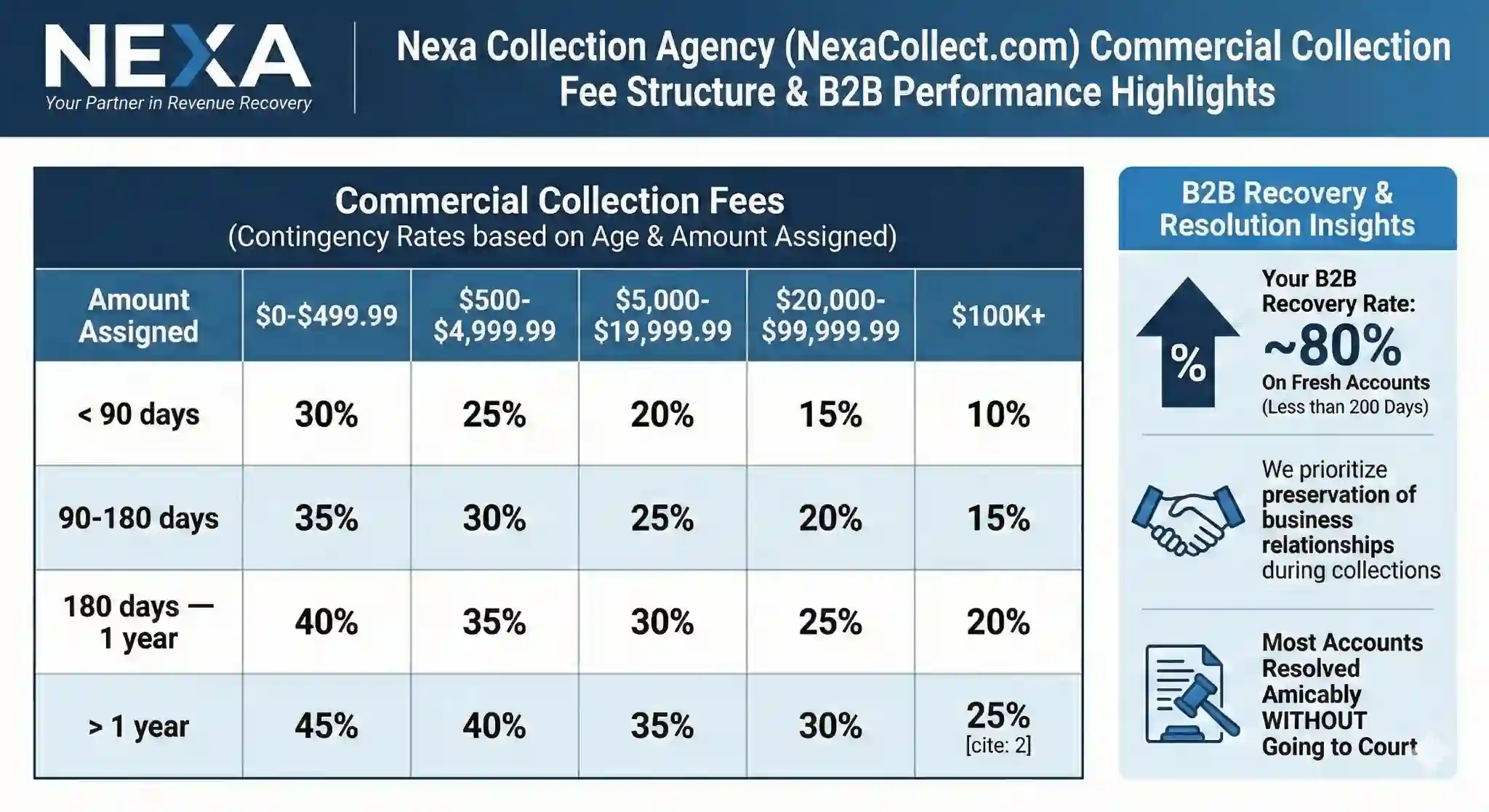

High Success Rate: While industry averages sit between 15% to 40%, we achieve a nearly 80% success rate on viable debts (accounts under 300 days old backed by solid documentation). Fee communicated in advance after reviewing your case. Results may vary as viability depends on documentation, debtor solvency and dispute status.

-

Business Credit Reporting: We report unpaid accounts to major Business Credit Bureaus. This affects the debtor’s ability to get future financing, creating a powerful incentive to pay you.

-

No Risk Pricing: We operate on a contingency basis—No Recovery, No Fee.

-

Nationwide Compliance: Backed by over 20 years experience, we are licensed in all 50 states and strictly follow the Uniform Commercial Code (UCC) and TCPA regulations.

- Credentials: Collections performed by ACA compliant collectors who are fully licensed to collect in all 50 states. HIPAA, NFIB, PCI and SOC type 2 compliant collection agency.

The “Velvet Hammer” Approach for B2B

A business debtor is often also a potential future client. We understand that preserving the business relationship is critical. Our collectors use a “Velvet Hammer” strategy: we are persistent and firm regarding the financial obligation, but professional and respectful in our communication. This approach recovers your money while leaving the door open for future business.

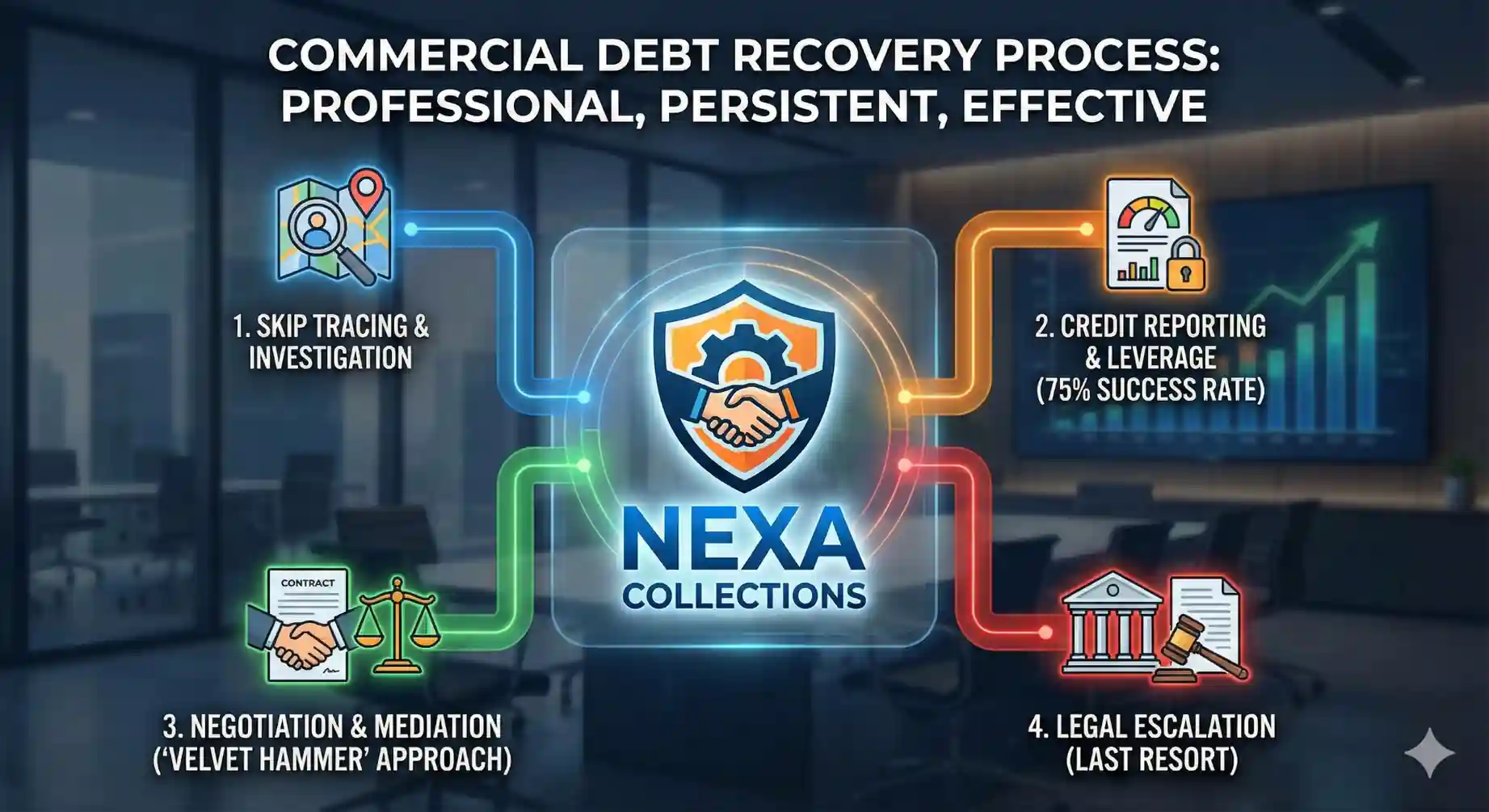

Our 4-Step Commercial Recovery Process

Our commercial debt collectors utilize persistent contact, credit leverage, and skilled negotiation to resolve the vast majority of cases amicably, reserving legal action strictly as a last resort.

1. Investigation & Skip Tracing

Before making the first call, we investigate. We verify business status, identify key decision-makers (owners, CFOs), and check for bankruptcy filings. If a debtor has “ghosted,” our skip tracing tools locate them.

2. Strategic Demands & Credit Reporting

We use a multi-channel approach (calls, emails, and mailed notices). Crucially, we utilize credit leverage:

Impact: A negative mark on a business credit report (such as D&B, Experian, or Equifax) can block a company from getting loans or vendor credit. This pressure often forces immediate payment.

3. Negotiation & Mediation

Commercial debts often involve disputes over service quality or contract terms. Our specialists act as mediators to cut through excuses and secure full payment or enforce a structured settlement plan.

4. Legal Escalation (With Your Approval)

If a debtor has assets but refuses to pay, we can forward the case to our affiliated network of commercial litigation attorneys. We handle the paperwork and manage the process, so you don’t have to.

| Need a Commercial Collection Agency? Serving Nationwide – Low Fee |

Industries We Specialize In

Commercial debt requires industry-specific knowledge. We have dedicated teams for:

-

Construction & Contractors: Handling liens, material disputes, and general contractor issues.

-

Manufacturing & Logistics: Collecting on unpaid freight bills, warehousing fees, and supply orders.

-

Staffing & SaaS: Recovering service fees and contract buyouts.

-

Wholesalers & Distributors: Managing high-volume, low-balance delinquent accounts.

- Commercial / Office leases

Commercial Collection Agency vs. Attorney vs. In-House AR Team

Not sure which path is right for your unpaid B2B invoice? Here’s how the three most common options compare:

| Factor | Collection Agency | Commercial Attorney | In-House AR Team |

|---|---|---|---|

| Cost | Contingency only (15–40%). No upfront fee. | Hourly ($250–$500/hr) + court costs. High upfront risk. | Salaried staff cost. Consumes internal resources. |

| Speed | 30–90 days for most cases | 6–18 months if litigation required | Varies; often slow due to competing priorities |

| Relationship Impact | Low — professional, diplomatic approach preserves the relationship | High — legal action typically ends the business relationship | Moderate — awkward for staff managing existing accounts |

| Legal Authority | None directly; escalates to attorneys when needed | Full legal authority — can sue, lien, garnish wages | None |

| Best For | Debts of any size; first recovery attempt; relationship-sensitive accounts | Large debts ($50K+) where debtor has assets and refuses all negotiation | Very recent invoices (under 30 days); ongoing client relationships |

| Credit Reporting | Yes — reports to D&B, Experian, Equifax Business | Only via court judgment | No |

Most businesses use a collection agency first — and only escalate to legal counsel if the agency recommends it based on debtor assets and dispute complexity.

Proven Results & Legal Authority

-

Midwest Logistics & Freight ($140,000): Resolved a complex cross-border brokerage dispute in 22 days via targeted mediation, bypassing months of litigation.

-

Industrial Manufacturing ($210,000): Recovered 100% of principal plus interest in under 45 days using “Corporate Diplomacy” to reconnect with new decision-makers after a client’s restructuring.

-

Commercial HVAC Construction ($68,000): Secured a full retention payment in 24 days. By filing a “Notice of Intent to Lien,” we forced a developer to release funds to protect their property title.

Our Technical Edge: B2B Security

Secured Creditor Leverage: We specialize in UCC-1 filings and Mechanic’s Liens to “perfect” your security interests. This expertise ensures your business is moved to the front of the line during payment disputes or insolvency proceedings, providing the highest level of legal protection available.

Checklist: What We Need to Start

To achieve that 75% success rate, providing the right documentation is key. When you place an account, we recommend uploading:

-

Copies of the original Invoices.

-

The signed Contract, Purchase Order (PO), or Service Agreement.

-

Statement of Account (showing payment history).

-

Any relevant email correspondence regarding the debt.

Frequently Asked Questions: Commercial Debt Collection

What is the difference between consumer and commercial collections?

Consumer collections (B2C) are strictly regulated by the Fair Debt Collection Practices Act (FDCPA) to protect individuals. Commercial collections (B2B) are governed by the Uniform Commercial Code (UCC) and contract law, allowing for different strategies — including business credit bureau reporting, UCC-1 filings, and mechanic’s liens — and often shorter timelines for resolution.

How much does a commercial collection agency charge?

We operate on a contingency fee model — no upfront cost, ever. Our rates typically range from 15% to 40% of the amount recovered, depending on the age of the debt, the balance size, and the complexity of the case. If we don’t collect, you pay nothing.

How long does commercial debt collection take?

Most commercial debts are resolved within 30–90 days. Simple cases with strong documentation (signed contracts, invoices, proof of delivery) can settle in 2–4 weeks. Complex disputes involving litigation or mediation can take 3–6 months. The sooner a past-due account is placed, the faster — and more likely — the recovery.

Can you collect business debts from companies in another state?

Yes. Nexa Collections is licensed in all 50 states and works with an affiliated network of commercial litigation attorneys nationwide. Interstate B2B collections are routine, and we are well-versed in the UCC provisions and contract law governing cross-border commercial disputes.

When is it too late to collect a commercial debt?

Every state has a statute of limitations for commercial contracts, typically 3 to 6 years. However, collection success drops significantly after 90 days — approximately 10% per additional month (Commercial Law League of America). Acting within 60–120 days of a missed invoice gives you the best chance of full recovery without litigation.

What is a UCC-1 filing and how does it help?

A UCC-1 (Uniform Commercial Code financing statement) is a legal notice filed with the state that establishes your interest in a debtor’s assets. Filing a UCC-1 effectively moves your business to the front of the repayment line if the debtor faces insolvency or asset liquidation — one of the most powerful tools in commercial debt recovery.

Do I need a lawyer to collect a commercial debt?

Not initially. A commercial collection agency resolves the majority of B2B debts through negotiation, credit leverage, and mediation — no litigation required. Legal escalation is reserved as a last resort for debtors who have assets but refuse to pay. In those cases, Nexa manages the entire legal escalation process through our attorney network.

Can you collect from a business that has closed down?

Difficult, but often possible. If the owner signed a personal guarantee, operates as a sole proprietor, or is part of a general partnership, they are personally liable. We also investigate for successor liability (reopened under a new name) and fraudulent transfers (hidden assets). Personal asset pursuit typically requires a court judgment via an affiliated attorney.

What is the average recovery rate for commercial collection agencies?

The industry average ranges from 15% to 40%. Nexa Collections achieves a nearly 80% success rate on viable claims — accounts under 300 days old backed by solid documentation. Results vary based on debtor solvency, dispute status, and documentation quality.

Is it worth hiring a collection agency for a small balance?

Yes — because reputable agencies work on contingency, you pay nothing unless money is recovered. Even balances under $5,000 are worth placing. The recovered funds go directly to your bottom line at zero upfront cost to you.

Ready to Boost Your Cash Flow?

Don’t let unpaid invoices sit on your books. Statistics show that after 90 days, the chance of collecting a debt drops by 10% every month.