In Iowa—from the advanced manufacturing plants of the Cedar Valley to the sprawling agricultural networks of the Des Moines metro—business is built on trust. When that trust is broken by unpaid debt, you need a partner who understands the Iowa Consumer Credit Code (ICCC).

Nexa provides 100% reputation-safe, compliant with the Iowa Attorney General’s notification requirements, equipped with all 50-state collections license, offering free credit reporting, free litigation/bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II & HIPAA compliant.

Need a Collection Agency? Contact us

The Iowa Legal Landscape

Iowa is a unique state for creditors. While it offers a long window to sue, it places strict annual limits on how much can be taken from a single debtor.

| Debt Type | Statute of Limitations | Iowa Code (IC) |

| Written Contracts | 10 Years | IC § 614.1(5) |

| Oral/Open Accounts | 5 Years | IC § 614.1(4) |

| Medical Debt | 5 Years | IC § 614.1 |

| Wage Garnishment | ALLOWED (Annual Caps) | IC § 642.21 |

Key Iowa Rules:

-

The 10-Year Window: Iowa offers one of the longest statutes of limitations in the U.S. (10 years for written contracts), allowing Nexa to recover “zombie debt” that other agencies have given up on.

-

Garnishment Caps: Iowa limits garnishment based on annual income (e.g., if a debtor makes less than $12,000/year, you may only be able to garnish $250 annually). Nexa’s “Iowa Desk” uses automated income verification to stay within these legal bounds.

-

Notification Threshold: Iowa’s unique annual garnishment caps (IC § 642.21) act as a strict legal “speed limit,” allowing creditors to garnish as little as $250 per year if a debtor earns under $12,000, while 2026 shifts have pushed the Iowa Attorney General’s notification threshold to $73,400 (as of Jan 2025)—meaning any agency collecting above this amount without state registration is operating illegally and exposing your business to penalties.

Cost-Effectiveness: The Nexa Advantage

-

Fixed-Fee Recovery ($15/account): Ideal for early-stage receivables. Debtors pay 100% directly to you.

-

Contingency Service (20%–40%): Performance-based recovery. If we don’t collect, you don’t pay. No recovery, no fee.

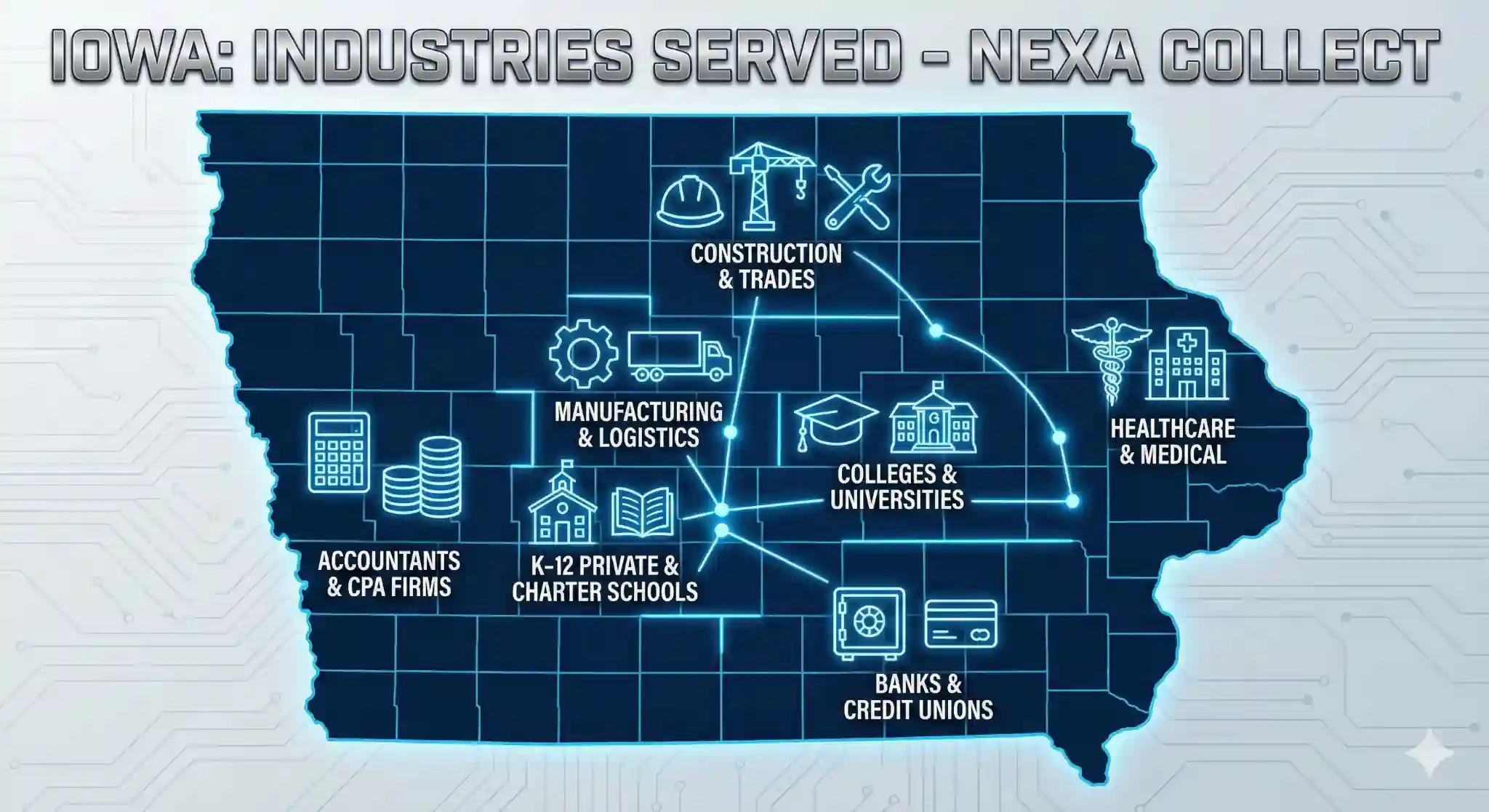

Industries We Serve in Iowa

-

Manufacturing & Industrial: B2B recovery for the machinery and food processing sectors. We handle high-value disputes for suppliers in the “Cultivation Corridor.”

-

Healthcare & Medical: 100% HIPAA-compliant. We manage patient balances while ensuring compliance with Iowa’s strict Debt Collection Practices Act to protect your clinic’s reputation.

-

Colleges & Universities: From major state institutions to private colleges, we manage tuition recovery and housing balances with a diplomatic approach that preserves student relationships.

-

K-12 Private & Charter Schools: Managing unpaid enrollment and textbook fees. We offer a family-sensitive mediation style tailored for Iowa’s local communities.

-

Accountants & CPA Firms: Recovery of professional service fees. We understand the Iowa tax cycle and recover your fees without damaging long-term client trust.

-

Banks & Credit Unions: Expert handling of delinquent consumer loans and deficiency balances. We utilize Iowa’s legal judgment tools to secure repayment on high-risk portfolios.

-

Construction & Trades: Revenue recovery for HVAC, electrical, and general contractors. We are experts in Iowa Code Chapter 572 (Mechanic’s Liens).

-

Restoration & Waste Management: Specialized B2B and B2C recovery for emergency service providers and environmental firms across the state.

Recent Iowa Recovery Results

Case 1: Des Moines Specialty Surgical Center (Medical)

-

The Problem: $92,000 in aging patient debt, much of it over 3 years old.

-

The Result: Nexa recovered $64,000 in 120 days using a “soft-touch” mediation strategy that resulted in zero complaints to the Attorney General.

Case 2: Cedar Rapids Construction Supplier (B2B)

-

The Problem: A $35,000 unpaid invoice for materials. The debtor was ignoring all calls.

-

The Result: Nexa’s legal team filed a Chapter 572 notice, resulting in a full $35,000 recovery plus interest within 45 days.

Frequently Asked Questions (FAQ)

Is Iowa medical debt currently exempt from credit reporting?

Not through any Iowa-specific law. Iowa doesn’t have its own state ban on medical debt credit reporting. A federal rule that would have removed medical debt from credit reports nationwide was vacated by a federal court in July 2025 and never took effect, so credit reporting on Iowa medical debt remains legally available where it otherwise qualifies.

Does it matter whether a patient signed a financial responsibility form, for statute-of-limitations purposes?

It can. Medical debt backed by a signed financial responsibility form is often treated under the 10-year written-contract rule, while a balance with no signed agreement is more likely to fall under the 5-year rule that generally applies to medical debt. The paperwork behind a balance matters as much as the type of care provided.

Are dental payment plans treated differently than a single visit bill under Iowa’s statute of limitations?

Often yes. A signed orthodontic or treatment-plan financing agreement tends to look more like a written contract with a longer window, while an unsigned running balance from routine visits is more likely treated under the shorter rule. Reviewing what was actually signed matters more than assuming every dental balance is treated the same way.

Is a personal guarantee on a commercial lease treated as a written contract for Iowa’s 10-year statute of limitations?

Generally yes, if the guarantee itself is a signed written document — it’s typically treated the same as other written contracts, giving a landlord or commercial creditor the full 10-year window.

Does Iowa’s consumer credit code protect a small business owner collecting on their own invoices, or only third-party agencies?

Both, generally. The debt collection provisions within the Iowa Consumer Credit Code apply broadly enough to cover original creditors collecting their own accounts, not just third-party collection agencies, so a business owner calling about an unpaid invoice is held to similar standards around harassment and misleading representations.

If a small business owner threatens “legal action” in a text message but hasn’t actually filed suit, is that a problem in Iowa?

It can be. Wage garnishment and most enforcement tools require a court judgment first — implying that legal consequences are already underway when no lawsuit has been filed can cross into a false or misleading representation under Iowa and federal law.

If a restoration or construction contractor misses the 90-day mechanic’s lien window, is the lien right gone for good?

Not necessarily, which surprises a lot of contractors used to stricter states. Iowa Code § 572.9 allows a lien to be posted up to roughly two years and 90 days after the last labor or materials were furnished — filing within the first 90 days just preserves maximum priority over other liens and purchasers. Missing 90 days costs priority, not the lien itself.

Does the mechanic’s lien clock restart if a contractor makes a brief return visit to fix a small issue?

Not automatically. Iowa courts have been clear that a minor visit made mainly to restart the filing deadline doesn’t count — the work has to be a genuine, substantive continuation of the job for the clock to reset from that later date.

Can an Iowa school withhold transcripts over unpaid tuition?

Many schools do withhold transcripts or records for unpaid balances as institutional policy, though this is generally a matter of the school’s own enrollment agreement rather than a specific Iowa statute, and practices vary between K-12 schools, colleges, and universities.

Does the Iowa Attorney General’s debt-collector notification threshold stay the same every year?

No — it’s tied to a federal Regulation Z threshold that adjusts annually, so the exact dollar figure changes from year to year rather than staying fixed. Always worth confirming the current year’s number directly with the Attorney General’s office rather than relying on a figure from a prior year.

How long does an Iowa court judgment last before a creditor loses the ability to collect?

About 20 years, and it can potentially be renewed beyond that — a separate, much longer clock than the original statute of limitations on the underlying debt. Once a creditor has an actual judgment, the collection window resets.

Popular Cities: